I’ve been adding Amazon (AMZN) to my portfolio in the past week; it is a bargain at $202, having dropped almost 20% from its high of $242.

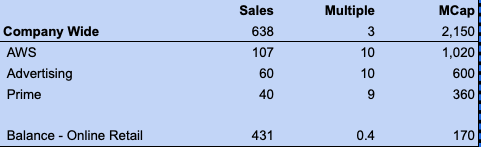

Amazon has 4 businesses.

Amazon Web Services

AWS is a cloud services behemoth and market leader with $ 108 Bn in 2024 sales, and still growing at 19%. That is remarkable growth for a market leader of that size with two other 800-pound Gorillas, Alphabet and Microsoft, chasing it. It generated operating profits of $39 Bn last year, a growth of 66% with an operating profit margin of 37%. This is Amazon’s most profitable segment and the growth engine, which powers everything.

Advertising

Amazon includes its advertising revenues in the online retail sales segment, but its advertising revenue last year was estimated between $ 56 Bn to $ 64 Bn in 2024, growing around 20% a year. This is also a high operating margin business, generating over 20% in operating profits.

Prime Subscriptions

Amazon doesn’t disclose its Prime subscriber numbers, but we estimate about 200Mn subscribers, including 180Mn in the US in 2024, generating over $40Bn in revenue.

This is another sustainable, sticky, and high-margin business, I’d value it at about 9x sales or $360 Bn.

I used a 9-10x multiple for the high-growth, high-profit margin, and sustainable businesses.

Online and physical retail sales in the US and abroad

These include third-party sales. Physical sales revenues are minuscule compared to total retail sales; loss leaders to expand reach and for analytic purposes, including in the online retail business. Amazon had a whopping $ 431 Bn in 2024. While online domestic and international sales are a drag, growing slower in single digits, they’re not significantly slower than Walmart’s sales growth and margins.

Amazon Segment Sales: Sources Amazon

Based on the Sum of the Parts schedule above, we’re getting the online and physical retail operations of $431 Bn at a market cap of just $170 Bn. The multiple of 0.4 is much lower than Walmart’s multiple of 0.74, or 40%.

Amazon has been spending heavily on Capex for AI to gear AWS and expand its web service offerings. In this arms race, they are scheduled to spend $100 Bn in 2025 to maintain and possibly expand their leadership.

We haven’t even valued all their investments and partnerships under AI development. That can be very valuable in the future.

I sold 15-25% of several stocks on Friday, 02/21/2025 as a de-risking exercise in the wake of weakening economic indicators, which I wrote about in this article.

Here’s the list and you can see them in the Trade Alerts Section as well.

ARISTA NETWORKS (ANET) $101

ADVANTEST CORP SPON ADR (ATEYY) $63

AMAZON INC (AMZN) $218

APPLIED MATERIALS INC COM (AMAT) $174

APPLOVIN CORP COM CL A (APP) $430

ARM HOLDINGS PLC (ARM) $147

BROADCOM INC COM (AVGO) $222

DOORDASH (DASH) $201.65

DUOLINGO INC CL A COM (DUOL) $410

DUTCH BROS INC CL A (BROS) $80

GITLAB INC CLASS A-COM (GTLB) $65.75

KLAVIYO INC (KVYO) $42.75

MICRON TECHNOLOGY INC (MU) $101

NETFLIX (NFLX) $1,012

SAMSARA INC (IOT) $54.25

SPOTIFY TECHNOLOGY S.A. COM (SPOT) $626

Earnings alone won’t save this market from a correction

Earnings season for Q4-2024 is mostly over except for Nvidia (NVDA), which reports on 02/26. M-7, and overall earnings were mostly lackluster and while most beat sandbagged estimates as always, the beats were nothing to write home about.

Instead, there was a lot of pressure for Q4 earnings to outperform to trump bearish indicators such as stubborn inflation, high valuations, tariff uncertainty, the likelihood of no interest cuts in 2025, difficult housing markets with 7% mortgage rates, weakening consumer sentiment, and so on….

Analysts, according to FactSet are still forecasting an estimated $268-$275 in 2025 S&P 500 earnings (about 11.5% growth), but this number seems more and more likely to either come in at the lower end or be revised lower as the year progresses. Second – the two-year back-to-back gains of 23% are a historical anomaly so I have to keep that in mind of a likely down year or a flat to 7-8% gain from already high levels.

Against all that is the $320Bn in Capex from the hyperscalers (That’s real money, not an economic survey or estimate – therefore the strongest catalyst ), which is extremely good for the AI industry and a very strong and vocal belief in the fundamentals – longer term we are on solid footing, and the AI story is just beginning, there are a lot of benefits to reap.

Active Risk Manangment

In short – a balancing act, which means there has to be active risk management. And especially when almost all the economic indicators came worse than expected, with sticky inflation and slower growth – stagflation. The Michigan survey of inflation expectations is followed closely by the Feds, and the weakening PMIs coincide with Walmart’s lower guidance. The reports have a lot of meat and don’t paint a pretty picture.

I’m not selling/trading the index or the stalwarts like Apple (AAPL), and Alphabet (GOOG) – there will be a flight to quality, thus not recommended. Even with a correction I don’t see the S&P 500 falling beyond 5,600-5,780. 5,780 was the Nov 5th election day level, that’s just 3.8% lower, not worth it.

My portfolio is tech-centric, and sometimes the drops in those are between 20% and 30% – AppLovin (APP), Palantir (PLTR), and Duolingo (DUOL) are examples, plus they’ve performed far better than expectations so taking some off is a great de-risking strategy for me.

I’ve owned it for over two years but will pyramid (add smaller quantities on a large base) it further.

Why is this company still worth investing in after a 20% post-earning bump?

Four important catalysts

Databricks partnership: The partnership with Databricka, which is much better known and valued increases brand awareness and opens a lot of new opportunities and doors.

This could accelerate growth from the current 22-23%.

Strong customer base: 90% of its revenues are coming from 100K + ARR clients.

The $1Mn+cohort saw the highest growth, and Confluent managed a net ARR of 117%, indicating strong upselling.

A changing data processing market: The entire batch processing model could be up for grabs – customers moving at the speed of light and willing to pay for the latest technology could be a huge TAM.

This is a paradigm shift, which Confluent has been trying to build into for a decade. 2025 might be that inflection year, with all the AI build-outs and use cases that are likely to need live processing – Confluent is the leader in that field. To be sure it’s not going to throw data processing models into obsolescence, why would you spend money on data that doesn’t need to be processed in real-time, but could take a large chunk of that market?

Snowflake acquiring RedPanda: Snowflake is reportedly trying to buy streaming competitor RedPanda for about 40x sales: While it’s not an obvious comparison, Red Panda is supposedly less than 10% of Confluent’s revenues but growing at 200-300%. But it’s the synergy with the larger data provider that’s getting it a massive price tag – Snowflake would love to have this arrow in its quiver of data tools.

Confluent is best positioned to take advantage of the possible shift from batch processing to processing in data streaming; its founders invented Apache Kafka, the open-source model for data streaming. And while its own invention is available for free – managing and maintaining it at scale needs the paid version. Over the years with the focus on Confluent Cloud, Confluent gets 90% of its $1Bn revenue from customers over $100K in annual revenue.

Confluent has the cash the tech chops and the focus – sure Apache Kafka is open source and many cloud service providers like AWS and Microsoft also provide enough competition, but no one has the product breadth that Confluent does.

I would not be surprised if Confluent’s multiple expands from the current 8x sales after this earnings call.

Here are the details of the December 2024, 4th quarter earnings:

Q4 Non-GAAP EPS of $0.09 beat by $0.03.

Revenue of $261.2Mn (+22.5% Y/Y) beat by $4.32Mn.

Q4 subscription revenue of $251Mn up 24% YoY

Confluent Cloud revenue of $138Mn up 38% YoY

2024 subscription revenue of $922Mn up 26% YoY

Confluent Cloud revenue of $492Mn up 41%YoY

1,381 customers with $100,000 or greater in ARR, up 12% YoY.

194 customers with $1Mn or greater in ARR, 23% YoY.

The Software Multiplier Effect: An interesting note from Wedbush’s Dan Ives on Artificial Intelligence, who believes that software AI players will likely get 8 times the revenue of hardware sellers. I.e., a multiplier effect of 8:1 from software.

He is directionally right, and I do agree with him about the multiplier effect of software, services, and platforms on top of hardware sales. I had done a primary study several years ago with companies like Oracle, IBM, and Salesforce among others, and we saw similar feedback of about 6 to 1 for software spend to hardware spend, over time. People naturally cost more.

Nonetheless, regardless of whether it is 6 to 1 or 8 to 1, both numbers are huge and extremely likely in my opinion in the next 5 to 10 years and Palantir’s (PLTR) Dec quarter earnings hit it out of the park.

Dan Ives said:

Palantir Technologies (NASDAQ:PLTR) and Salesforce (NYSE:CRM) remain the two best software plays on the AI Revolution for 2025.

The firm also recommended other software vendors such as Oracle (ORCL) IBM (IBM), Innodata (INOD) Snowflake (SNOW), MongoDB (MDB), Elastic (ESTC), and Pegasystems (PEGA) enjoying the AI spoils.

Analysts led by Daniel Ives said:

Palantir has been a major focus during the AI Revolution with expanding use cases for its marquee products leading to a larger partner ecosystem with rapidly rising demand across the landscape for enterprise-scale and enterprise-ready generative AI.

Major Growth Expected: The analysts added that this will be a major growth driver for the U.S. Commercial business over the next 12 to 18 months as more enterprises take the AI path with Palantir. They believe “Palantir has a credible path to morph into the next Oracle over the coming decade” with Artificial Intelligence Platform, or AIP, leading the way.

Wedbush’s feedback about budget allocations is very helpful and even if one discounted Dan Ives’ perpetual optimism and bullishness by some, it’s a great indicator that this will be a favored sector in 2025-2028.

Ives and his team have been tracking several large companies that are or are planning to use AI path in 2025 to gauge enterprise AI spending, use cases, and which vendors are separating from the pack in the AI Revolution.

The numbers are gratifying:

Analysts expect that AI now consists of about 10% of many IT budgets for 2025 they are tracking and in some cases up to 15%, as many chief information officers, or CIOs, have accelerated their AI strategy over the next six to nine months as monetization of this key theme is starting to become a reality across many industries.

“While the first steps in AI deployments are around Nvidia (NVDA) chips and the cloud stalwarts, importantly we estimate that for every $1 spent on Nvidia, there is an $8-$10 multiplier across the rest of the tech ecosystem,” said Ives and his team.

What’s more important?

Analysts noted that about 70% of customers they have talked to have accelerated their AI budget dollars and initiatives over the last six months. The analysts added that herein is the huge spending that is now going on in the tech world, with $2T of AI capital expenditure over the next three years fueling this generational tech spending wave.

Hyperscalers indicated supreme confidence in their AI strategy committing in excess of $300Bn in Capex for 2025, which is historic. Amazon’s CEO Any Jassy was categorical in stating AWS doesn’t spend till they’re certain of demand.

Ives had this to add, underscoring Amazon’s confidence.

In addition, Ives and his team said that they are seeing many IT departments focused on foundational hyperscale deployments for AI around Microsoft (MSFT) Amazon (AMZN), and Google (GOOG) (GOOGL) with a focus on software-driven use cases currently underway.

“The AI Software era is now here in our view,” said Ives and his team. Wedbush’s team strongly believes that the broader software space will expand the AI revolution further, cementing what I saw at the CES last month. There is so much computing power available and so many possibilities of use cases exploding that this space could see a major inflection point in 2025-2026.

Large language models, or LLM, and the adoption of generative AI should be a major catalyst for the software sector.

I missed buying this in the low 90s, waiting to see if their transformation to an AI chip company was complete. Having a cyclical past, with non-performing business segments made me hesitate, besides far too many promises have been made in the AI space only for investors to be disappointed.

Marvel has been walking the talk, Q3 results in Dec 2024 were exemplary, and guidance even better.

Hyperscaler demand

With a planned Capex of $105Bn for 2025, Amazon confirmed on their earnings call that the focus will continue on custom silicon and inferencing. Amazon and Marvell have a five-year, “multi-generational” agreement for Marvell to provide Amazon Web Services with the Trainium and Inferentia chips and other data center equipment. Since the deal is “multi-generational,” Marvell will continue to supply the released Trainium2 5nm (Trn2) while also supplying the newly-announced Trainium3 (Trn3) on the 3nm process node expected to ship at the end of 2025. Amazon is an investor in Anthropic with plans to build a supercomputing system with “hundreds of thousands” of Trainium2 chips called Project Rainier. The DeepSeek aftermath does suggest a further democratization of AI, as inference starts gaining prominence from 2026.

Critically, like other hyperscalers Microsoft, Meta, and Alphabet, Amazon announced a high Capex (Capital Expenditure) plan of $105Bn for 2025, 27% higher than 2024, which itself was 57% higher than the previous year, for AI cloud and datacenter buildout. It was the last of the big four to confirm that massive AI spending was very much on the cards for 2025.

Here’s the scorecard for 2025 Capex, totaling over $320Bn. A few months back, estimates were swirling for $250 to $275. Goldman had circulated $300Bn in total Capex for the year, and these four have already planned more.

Amazon $105Bn Microsoft $80Bn Alphabet $75Bn Meta $60 to $65Bn Total $320Bn

The earnings call discussed DeepSeek R1 and the lower AI cost structure that it may presage, with the possibility of lower revenue for AI cloud services.

“We have never seen that to be the case,” Amazon CEO Andy Jassy said on the call. “What happens is companies will spend a lot less per unit of infrastructure, and that is very, very useful for their businesses. But then they get excited about what else they could build that they always thought was cost prohibitive before, and they usually end up spending a lot more in total on technology once you make the per unit cost less.” Amazon plans to spend heavily on custom silicon and focus on inference as well besides buying Blackwells by the truckload.

Q3-FY2025

Marvell reported impressive Q3 results that beat revenue estimates by 4% and adjusted EPS estimates by 5.5%, led by strong AI demand. FQ3 revenue accelerated to 6.9% YoY and 19.1% QoQ growth to $1.52 billion, helped by a stronger-than-expected ramp of the AI custom silicon business.

For the next quarter, management expects revenue to grow to 26.2% YoY and 18.7% QoQ to $1.8 billion at the midpoint. The Q4 guide beats revenue estimates by 9.1% and adjusted EPS estimates by 13.5%. Management expects to significantly exceed the full-year AI revenue target of $1.5 billion and indicated that it could easily beat the FY2026 AI revenue target of $2.5 billion.

Marvell has other segments, which account for 27% of the business that are not performing as well, but they’re going full steam ahead to focus on the custom silicon business and expect total data center to exceed 73% of revenue in the future.

Adjusted operating margin – 29.7% V 29.8% last year, and better than the management guide of 28.9%.

Management guidance for Q4 is even higher at 33%.

Adjusted net income – $373 Mn or 24.6% of revenue compared to $354.1 Mn or 25% of revenue last year.

Management has also committed to GAAP profitability in Q4, and continued improvements.

Custom Silicon – There are estimates of a TAM (Total Addressable Market) of $42 billion for custom silicon by CY2028, of which Marvell could take 20% market share or $8Bn of the custom silicon AI opportunity, I suspect we will see a new forecast when the company can more openly talk about an official announcement. On the networking side, the TAM is another $31 billion.

“Oppenheimer analyst Rick Schafer thinks that each of Marvell’s four custom chips could achieve $1 billion in sales next year. Production is already ramping up on the Trainium chip for Amazon, along with the Axion chip for the Google unit of Alphabet. Another Amazon chip, the Inferentia, should start production in 2025. Toward the end of next year, deliveries will begin on Microsoft’s Maia-2, which Schafer hopes will achieve the largest sales of all.”

Key weaknesses and challenges

Marvell carries $4Bn in legacy debt, which will weigh on its valuation.

The stock is already up 70% in the past year, and is volatile – it dropped $26 from $126 after the DeepSeek and tariffs scare.

Custom silicon, ASICs (Application Specific Integrated Circuits) have strong competition from the likes of Broadcom and everyone is chasing market leader Nvidia. Custom silicon as the name suggests is not widely used like an Nvidia GPU and will encounter more difficult sales cycles and buying programs.

Drops in AI buying from data center giants will hurt Marvell.

Over 50% of Marvell’s revenue comes from China, and it could become a victim of a trade war.

Valuation: The stock is selling for a P/E of 43, with earnings growth of 80% in FY2025 and 30% after that for the next two years – that is reasonable. It has a P/S ratio of 12.6, with growth of 25%. It’s a bit expensive on the sales metric, but with AI taking an even larger share of the revenue pie, this multiple could increase.

UiPath’s competitive edge lies in its AI integration, SAP partnership and industry-agnostic automation solutions, making it a strong contender in RPA despite generative AI threats.

Recent struggles were due to sales execution issues, and competition, but the company shows signs of recovery with strategic changes and a focus on large clients and collaborations.

Founder Daniel Dines’ return as CEO, workforce reductions, and strategic partnerships, especially with SAP, are pivotal in steering UiPath back on track.

Despite current challenges, UiPath’s strong cash position, cost-saving measures, and promising AI Agentic capabilities make it a worthwhile investment with limited downside risk.

UiPath’s (PATH) updated financial forecast and current valuation do make a great case for investment as a GARP, now that it’s likely to grow only in the mid-teens, valued at just 5X sales, and 25x adjusted earnings. Besides, cash flow is almost double the adjusted operating income, so that too is a plus. I own some and plan to accumulate on declines.

Roblox (RBLX) is a market leader for gaming apps and the short report from The Hindenburg. alleging irregularities in engagement metrics had a negligible impact on its share price.

In October 2024, Roblox shares dropped 9% after Hindenburg’s short thesis but quickly recovered, closing only 2% lower, highlighting investor resilience. The stock, which was coasting in the low forties then, has gained almost 50% since then to $58 today.

I believe it is a solid company. Although it is overpriced, it is worth considering as an investment if the price drops below $50.

Positives

Market Leader: Roblox is the number one grossing app for the iPad across the App Store, and regularly among the top 10 apps for the iPhone, across categories, according to data collected by Refinitiv.

Not gaming the market: Roblox also showed strong App Store momentum across some of the biggest gaming markets in the world, including North America, Europe, and SEA. I believe these gross numbers are extremely difficult if not impossible to fudge, instead it supports Roblox’s strong commercial value and future prospects.

Good quarterly numbers and guidance: Roblox’s booking in Q2 grew around 22% YoY, to $955Mn, and it guided to $1-$1.025Bn for Q3.

Partnering with Shopify: The commercial integration partnership with Shopify also helps Roblox further build out its virtual market, with better monetization opportunities.

Wall Street likes it: Ken Gawrelski, an analyst from Wells Fargo, maintained a Buy rating on Roblox, raising the price target to $58.00. He observes that the company’s strong engagement trends continue to outperform expectations, with a significant increase in concurrent users and app downloads, indicating robust user growth. These factors contribute to a raised third-quarter total bookings growth forecast, which is now expected to surpass the company’s guidance and the consensus estimates.

Great monetization tools: Roblox’s expansion of monetization tools, and strength in in-game spending is a significant competitive advantage for driving long-term developer and user engagement on the platform. Shopify and other initiatives are expected to enable developers to better monetize their offerings.

The trend is their friend: The strategic shift towards direct response advertising, including new partnerships and live commerce testing, indicates that Roblox can make the most of the new opportunities in digital advertising.

These initiatives give me confidence in the company’s sustainable long-term revenue growth.

Negatives

Hindenburg’s biggest grouse was the possibility of fudging and overstating user growth and engagement numbers, which though denied strongly by the company and discarded by analysts could create doubts about the valuation in the future.

Revenue growth forecasts for the next 3 years is around 16-18% and with the stock selling at 7.5x sales, it is expensive and a quarterly miss could lead to a large drop. Even the positive Wells Fargo analyst had a price target of $58, we’re already crossed that level.

It is loss-making on a GAAP basis with heavy stock-based compensation, which likely sets a cap on its valuation. That said cash flow is strong – around 19% of revenue.

Overall, Hindenburg didn’t make an impact, Roblox is performing well but I would be very careful about the price and get it lower to make a meaningful return.

Oracle (ORCL) $166 is a solid investment opportunity for 3-5 years, with a decent shot at growing data center cloud revenues faster than its other businesses, with a push from AI requirements from clients like Meta. Hyperscalers and cloud service providers are expected to spend a capex of $300Bn in 2025, boosting cloud infrastructure providers such as Oracle.

Oracle’s earnings should grow between 16-18% in the next 3-5 years- and it’s very reasonably priced at 24x forward earnings of $7.05.

Its 31% GAAP operating margins are another sign of strength, especially for a legacy/mature $52Bn+ tech company.

Revenues should grow at 12-14% annually in the next 3-4 years, which is impressive for a company of that size. Oracle’s P/S multiple is not expensive at 7X sales.

Oracle Cloud Infrastructure’s robust growth is a big catalyst for the company and the stock, and while the near-term Oracle’s FQ2 double miss disappointed investors, the price drop from $191 has created an opportunity for investors. Besides Oracle could gain market share over time.

Oracle’s modular approach and scalable infrastructure offer cost competitiveness, attracting customers. The company’s ability to scale AI clusters, demonstrated by the deployment of a 65,000 NVIDIA H200 supercomputer and a 336% surge in GPU consumption last quarter, further highlights its appeal.

Furthermore, Oracle’s strengthened partnership with Meta for AI training underscores its attractiveness to both large enterprises and smaller businesses. This reinforces the effectiveness of Oracle’s modular strategy, which aims to provide customers with an improved total cost of ownership (TCO) compared to leading hyperscaler competitors.

Their overall cloud segment is about 55% of revenues and growing at 25%, but the licensing segment has been stagnant for the past two years. Over time this will tilt more decisively towards the cloud, allowing them to either increase or maintain their multiples/valuation.

Broadcom (AVGO) reported good results and exceeded guidance for Q1-FY2025

Revenue $14.05Bn for Q4-FY2024, up 51% YoY (It acquired VMWare) in line with expectations. Without the VMWare acquisition, organic revenue growth was 11%.

GAAP net income of $4.3Bn; Non-GAAP net income of $ 6.9Bn, slightly higher than estimated.

Adjusted EBITDA of $9.1Bn or 65 percent of revenue – Adjusted margins are high because of the non-cash adjustment of charges for the merger with VMWare.

GAAP diluted EPS of $0.90 for the fourth quarter; Non-GAAP diluted EPS of $1.42 for the fourth quarter – Slightly higher than estimates.

Solid Cash Generation: Cash from operations of $5.6Bn for the fourth quarter, less capital expenditures of $122Mn, resulted in $5.5Bn of free cash flow, or 39 percent of revenue.

First quarter fiscal year 2025 revenue guidance of approximately $14.6Bn, an increase of 22 percent from the prior year period – Slightly higher than estimates of $14.5Bn.

First quarter fiscal year 2025 Adjusted EBITDA guidance of approximately 66 percent of projected revenue.

Surging AI revenues: It exceeded its earlier projection of $11.5Bn AI revenues with $ 12.2Bn, mainly with sales of ASICs to Google, besides selling ethernet solutions to other AI data center clients.

“Broadcom’s fiscal year 2024 revenue grew 44% year-over-year to a record $51.6 billion, as infrastructure software revenue grew to $21.5 billion, on the successful integration of VMware,” said Hock Tan, President and CEO of Broadcom Inc. (AVGO) “Semiconductor revenue was a record $30.1 billion driven by AI revenue of $12.2 billion. AI revenue which grew 220 percent year-on-year was driven by our leading AI XPUs and Ethernet networking portfolio.“

Should the proposed development of semis for Apple go through as planned, they’d be an even stronger contender in AI data center infrastructure.

I own Broadcom and continue to accumulate and plan to hold for at least 3-5 years. The VMWare integration is also going according to plan and will be a source of sustainable and recurring revenue.

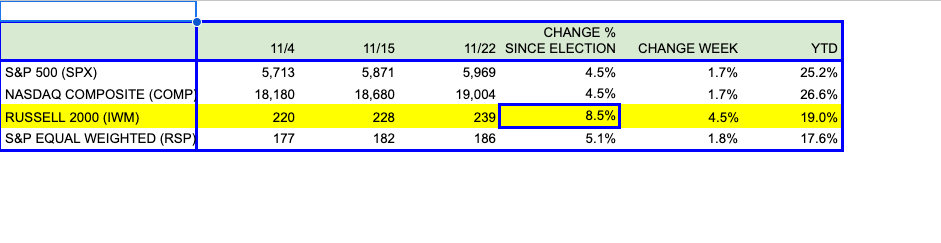

The Russell 2000 (IWM) ETF and the S&P 500 Equal Weighted Index have been outperforming the S&P 500 and the NASDAQ Composite since the election. Last week was no exception.

The IWM comprises 2,000 of the smallest capitalized companies in the market.

The IWM has gained 8.5% compared to the S&P 500’s and the Nasdaq Composite’s 4.5% gain since Nov 4th, 2024, and 4.5% in the last week, significantly higher than the 1.7% each gained by its larger counterparts.

Last week, breadth was better across the board. The NYSE Advance/Decline Ratio or $ADRN, finished on Friday 11/22 at 3.6, (3.6 stocks advancing V 1 decline), it averaged 2.29 for the past week, and 1.81 since the Nov 5th election against an average of 1.61 for the Year To Date.

Clearly, everyone wants in and has been wanting in since the election – money has shifted from chasing the M-7 and other large caps to a larger pool of small-cap stocks. The markets have aggressively seized that opportunity and have bid them faster than the large caps. Is the breadth a bullish sign or is the euphoria unsettling?

Let’s look at some of the main reasons:

Business-Friendly Populist Government: To some extent, there is a perception that small caps are closer to the economy than the M-7, and other tech behemoths, which explains why the prospects of tax cuts, pro-business policies,and less regulation would improve their fortunes much more than the large caps.

Small Caps are cheaper: Large-cap tech is also perceived to be much more expensive – the average earnings multiples are lower for small caps.

Everybody and their uncle owns Nvidia: Investors and traders are likely overexposed to big-tech stocks and need to diversify, but were afraid to do so. A Bank of America study found “Long M-7” the most crowded trade in the markets just two weeks back.

Animal spirits are up: More risk-taking, Hell the markets are likely to go up with the pro-market Trump administration and I should add. Consumer sentiment seems to have boomed since the election.

FOMO – The small caps are up and I don’t have exposure, I need to jump on this train.

Should we remain invested or does breadth call for caution?

Business-Friendly Populist Government: I agreewith the tax cuts and deregulation, but we need to see if the proposed tariff plans could derail this.

Small Caps are cheaper: Small caps may be cheaper, but if you take out the premium that should go to secular growers with sustainable competitive advantages, and look at the risks associated with smaller, struggling businesses, the difference is not that stark, and sometimes it’s the opposite. Some businesses are just terrible, with no competitive advantages, and low prospects of growth, and their stock prices are driven purely by momentum. These are risky businesses you don’t want to own, period. For now, I believe this rotation may continue for a few weeks more, but the bottom line — if I’m looking at a small cap or even a small cap index, I’m going to look at the underlying fundamentals before making a call. I’m not riding any gravy trains here.

Everybody and their uncle owns Nvidia: That is true – the overownership is well documented, and when there is overownership, the scope to continue rising is much, much lower. To some extent, the earnings have to catch up with the valuation or the stock will just drift, and you’ll find large-cap investors rotating into small-caps.

Animal spirits are up: Drill, Baby, Drill, DOGE, etc, all sound great during the honeymoon period, but the jury is still out, we’ll have to see how everything works in 2025. I’m on the fence on this, it’s still a show-me story, and the possibilities of this going south are not small.

FOMO: This I am seeing first hand – For example, Navitas (NVTS) one of my weak small-cap picks, which sank from $4 to $1.60, has suddenly bounced back from the dead to $2.40 in a week! I’m not going to look a gift horse in the mouth, I didn’t add but I’m hoping it bounces back to at least where I can exit. Navitas is actually in the right place at the right time – its focus is on power saving for data centers, which could be a huge business, but it’s currently, heavily exposed to China with 57% of sales there, (it is in 60% of all the cell phones in the world). Besides Navitas, several other stocks popped in the previous week, without any changes in fundamentals.

Conclusion

Breadth is good for the market, just not at the expense of the usual due diligence.

All five reasons helped a fundamentally sound, and highly high-quality small-cap stock like Confluent, (CFLT) a favorite, that I’ve owned and written about. It’s a $1Bn revenue company with an $8Bn market cap, which shot up from $27.50 to $31.50 in the past week for several reasons.

The business-friendly and animal spirits bounce – because now enterprises seem to be spending; The halo effect from Snowflake (SNOW) the 4x larger data warehousing, market leader had a great quarter and guidance last week; Confluent, which serves the same enterprise market with data streaming is also being seen as a beneficiary and now gets the higher multiple.

The over-ownership bounce: I would rather add more Confluent and Klaviyo (KVYO) shares because my portfolio already has high exposure to large caps.

Small Caps could continue to outperform in the near term, just to catch up. As we saw from the chart, on a YTD basis they’re still behind at 19% to 25%.