Oracle (ORCL) $166 is a solid investment opportunity for 3-5 years, with a decent shot at growing data center cloud revenues faster than its other businesses, with a push from AI requirements from clients like Meta. Hyperscalers and cloud service providers are expected to spend a capex of $300Bn in 2025, boosting cloud infrastructure providers such as Oracle.

Oracle’s earnings should grow between 16-18% in the next 3-5 years- and it’s very reasonably priced at 24x forward earnings of $7.05.

Its 31% GAAP operating margins are another sign of strength, especially for a legacy/mature $52Bn+ tech company.

Revenues should grow at 12-14% annually in the next 3-4 years, which is impressive for a company of that size. Oracle’s P/S multiple is not expensive at 7X sales.

Oracle Cloud Infrastructure’s robust growth is a big catalyst for the company and the stock, and while the near-term Oracle’s FQ2 double miss disappointed investors, the price drop from $191 has created an opportunity for investors. Besides Oracle could gain market share over time.

Oracle’s modular approach and scalable infrastructure offer cost competitiveness, attracting customers. The company’s ability to scale AI clusters, demonstrated by the deployment of a 65,000 NVIDIA H200 supercomputer and a 336% surge in GPU consumption last quarter, further highlights its appeal.

Furthermore, Oracle’s strengthened partnership with Meta for AI training underscores its attractiveness to both large enterprises and smaller businesses. This reinforces the effectiveness of Oracle’s modular strategy, which aims to provide customers with an improved total cost of ownership (TCO) compared to leading hyperscaler competitors.

Their overall cloud segment is about 55% of revenues and growing at 25%, but the licensing segment has been stagnant for the past two years. Over time this will tilt more decisively towards the cloud, allowing them to either increase or maintain their multiples/valuation.

Turnarounds rarely succeed. Ask Warren Buffet, who tried his best to turn around textiles major Berkshire Hathaway, which was suffering from a barrage of cheaper imports (sound familiar?) before giving up and turning it into the holding company and investment giant that is today. Rolls-Royce (RYCEY) is in the midst of one in the cutthroat world of aerospace engineering and manufacturing and is having a banner year with its stock up 82% to date.

Can it continue or sink under its three difficult cyclical segments, aerospace, defense, and power with low margins and tough competition? –

A year and a half ago, CEO Tufan Erginbilgic took over a struggling company with pandemic-induced challenges, operational inefficiencies, and persistent financial setbacks. His approach was bold and uncompromising: radical cost-cutting, operational streamlining, and a laser-focused strategy to transform Rolls-Royce’s fundamental business model. He did admirably, trimming the workforce by 6% and reducing expenses by £400 million. He also raised prices, optimized procurement processes, and renegotiated contracts.

As a result, in the first 6 months of 2024, Rolls-Royce did an excellent job with

19% revenue growth to £8.18Bn

74% increase in operating profit to £1.2Bn, with an OPM of 14%

Free cash flow improvement by 225% to £1.2Bn

Net debt reduced to its lowest level in five years to £822 million

The turnaround was led by Civil Aerospace (its largest division), and the strongest performer with 27% revenue growth, which benefited from post-pandemic air travel recovery. What’s more, its higher-margin service revenues also grew 27% to 68% of division sales, indicating a robust and recurring revenue stream. The aerospace segment benefited from strong growth in in-flight hours for engines under long-term service agreements, and large engine deliveries to OEMs increased by 4% with overall OEM deliveries up 26%.

Besides the volume growth, Rolls-Royce also passed on elevated costs, after successfully renegotiating long-term service agreements. Airbus, which saw increased demand for the Trent engines and General Dynamics for its Gulfstream engines, as big customers helped; Competitor General Electric saw its equipment sales fall year-on-year in the second quarter due to lower LEAP engine deliveries.

Defense and Power Systems also showed growth. Defense revenues grew 18%, with strong submarine platform sales and higher service revenue. Power Systems saw a smaller 6% revenue increase, mainly from Datacenters, a segment that certainly holds greater promise.

What does the future look like and can they continue with the turnaround?

Aerospace: Rolls-Royce exclusively provides the engines for the Airbus A350 and A330neo and those airplanes have seen some solid sales momentum which will drive value for the company. The services division will provide better margins

Defense: Given the stronger Republican emphasis on defense, I believe Rolls Royce should see better impetus from defense budgets in the next 4 years.

Power: Data center power needs should be a great opportunity for Rolls-Royce especially with the small modular reactor. The UK government has already picked Rolls-Royce as one of four sources, as has the Czech electricity company, CEZ.

Key Risks:

Execution challenges: This is not their first trip out of the despair well, and once the benefits from cost-cutting dissipate, they still have to grow.

Exposure to global air travel trends, which will slow down after the post-COVID revenge travel boom. Regional revenues were lower and didn’t participate in the post-COVID travel boom.

The company is worth buying: I plan to buy Rolls Royce on declines after such a large run-up for the following reasons.

Reasonable valuation for a GARP (Growth At A Reasonable Price): Analyst consensus estimates call for revenue growth of 8-10% for the next three years at a paltry P/S valuation of just 2.4x sales. Rolls-Royce is also slated to grow EPS by 20% in the next three and has a reasonable P/E of 26, or just 1.3.

Improving margins: Given the improvements in operating margins and the focus on efficiency, margins could improve further and help earnings grow.

Diversification: The company’s diversified portfolio – civil aerospace, defense, and power systems – helps hedge against sector-specific cyclicality.

Datacenter Opportunity: I also believe that Datacenter requirements for power will be a big winner for Rolls-Royce.

Dividends: They’re also reinstating dividends at 30% of after-tax profits, which should provide a floor for the stock price.

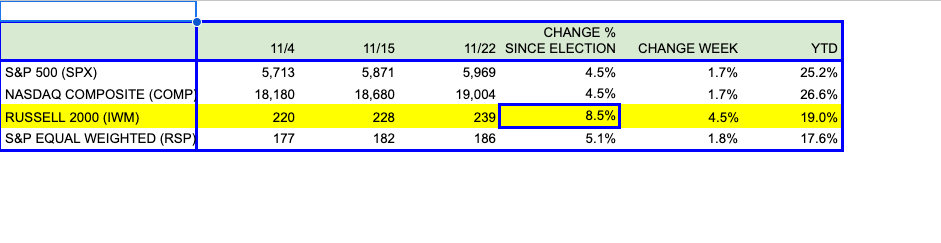

The Russell 2000 (IWM) ETF and the S&P 500 Equal Weighted Index have been outperforming the S&P 500 and the NASDAQ Composite since the election. Last week was no exception.

The IWM comprises 2,000 of the smallest capitalized companies in the market.

The IWM has gained 8.5% compared to the S&P 500’s and the Nasdaq Composite’s 4.5% gain since Nov 4th, 2024, and 4.5% in the last week, significantly higher than the 1.7% each gained by its larger counterparts.

Last week, breadth was better across the board. The NYSE Advance/Decline Ratio or $ADRN, finished on Friday 11/22 at 3.6, (3.6 stocks advancing V 1 decline), it averaged 2.29 for the past week, and 1.81 since the Nov 5th election against an average of 1.61 for the Year To Date.

Clearly, everyone wants in and has been wanting in since the election – money has shifted from chasing the M-7 and other large caps to a larger pool of small-cap stocks. The markets have aggressively seized that opportunity and have bid them faster than the large caps. Is the breadth a bullish sign or is the euphoria unsettling?

Let’s look at some of the main reasons:

Business-Friendly Populist Government: To some extent, there is a perception that small caps are closer to the economy than the M-7, and other tech behemoths, which explains why the prospects of tax cuts, pro-business policies,and less regulation would improve their fortunes much more than the large caps.

Small Caps are cheaper: Large-cap tech is also perceived to be much more expensive – the average earnings multiples are lower for small caps.

Everybody and their uncle owns Nvidia: Investors and traders are likely overexposed to big-tech stocks and need to diversify, but were afraid to do so. A Bank of America study found “Long M-7” the most crowded trade in the markets just two weeks back.

Animal spirits are up: More risk-taking, Hell the markets are likely to go up with the pro-market Trump administration and I should add. Consumer sentiment seems to have boomed since the election.

FOMO – The small caps are up and I don’t have exposure, I need to jump on this train.

Should we remain invested or does breadth call for caution?

Business-Friendly Populist Government: I agreewith the tax cuts and deregulation, but we need to see if the proposed tariff plans could derail this.

Small Caps are cheaper: Small caps may be cheaper, but if you take out the premium that should go to secular growers with sustainable competitive advantages, and look at the risks associated with smaller, struggling businesses, the difference is not that stark, and sometimes it’s the opposite. Some businesses are just terrible, with no competitive advantages, and low prospects of growth, and their stock prices are driven purely by momentum. These are risky businesses you don’t want to own, period. For now, I believe this rotation may continue for a few weeks more, but the bottom line — if I’m looking at a small cap or even a small cap index, I’m going to look at the underlying fundamentals before making a call. I’m not riding any gravy trains here.

Everybody and their uncle owns Nvidia: That is true – the overownership is well documented, and when there is overownership, the scope to continue rising is much, much lower. To some extent, the earnings have to catch up with the valuation or the stock will just drift, and you’ll find large-cap investors rotating into small-caps.

Animal spirits are up: Drill, Baby, Drill, DOGE, etc, all sound great during the honeymoon period, but the jury is still out, we’ll have to see how everything works in 2025. I’m on the fence on this, it’s still a show-me story, and the possibilities of this going south are not small.

FOMO: This I am seeing first hand – For example, Navitas (NVTS) one of my weak small-cap picks, which sank from $4 to $1.60, has suddenly bounced back from the dead to $2.40 in a week! I’m not going to look a gift horse in the mouth, I didn’t add but I’m hoping it bounces back to at least where I can exit. Navitas is actually in the right place at the right time – its focus is on power saving for data centers, which could be a huge business, but it’s currently, heavily exposed to China with 57% of sales there, (it is in 60% of all the cell phones in the world). Besides Navitas, several other stocks popped in the previous week, without any changes in fundamentals.

Conclusion

Breadth is good for the market, just not at the expense of the usual due diligence.

All five reasons helped a fundamentally sound, and highly high-quality small-cap stock like Confluent, (CFLT) a favorite, that I’ve owned and written about. It’s a $1Bn revenue company with an $8Bn market cap, which shot up from $27.50 to $31.50 in the past week for several reasons.

The business-friendly and animal spirits bounce – because now enterprises seem to be spending; The halo effect from Snowflake (SNOW) the 4x larger data warehousing, market leader had a great quarter and guidance last week; Confluent, which serves the same enterprise market with data streaming is also being seen as a beneficiary and now gets the higher multiple.

The over-ownership bounce: I would rather add more Confluent and Klaviyo (KVYO) shares because my portfolio already has high exposure to large caps.

Small Caps could continue to outperform in the near term, just to catch up. As we saw from the chart, on a YTD basis they’re still behind at 19% to 25%.

An interesting article in the Wall Street Journal discusses Google’s anti-trust case in more detail. Quoting from the article:

“Some of the DOJ’s proposals were expected, such as the divestiture of the Chrome browser and a ban on payments to Apple AAPL in exchange for default or preferred placement of Google’s search engine on Apple’s devices”, which are minor and something Google could take in its stride.

But the government’s proposal of “Restoring Competition Through Syndication And Data Access”, could be more harmful in the long run.

Restoring competition through access, which involves Google providing its search index—essentially the massive database it has about all sites on the web—to rivals and potential rivals at a “marginal cost.”, in my opinion, is stripping Google of its IP, and competitive advantages, which it has built through decades of human and monetary capital. It is draconian and a massive overreach. It gets worse, if the government has its way, Google would also have to give those same parties full access to user and advertising data at no charge for 10 years.

For now, it’s a wish list, a starting point of a high ask, which I’m sure the government expects to be whittled down to something less harmful and gives it some bragging rights.

Points to consider

This could harm/scare other tech giants.

The Turney Act makes this government agnostic, it guarantees judicial oversights for antitrust actions.

Alphabet has significant and solid resources and defensible arguments to fight this, mainly the 2 decades of resources put into building this moat.

The stock is likely to stay range-bound or sideways because of the legal issues, where most investors would likely be cautious, even though this morning itself there have been strong buy calls from analysts.

I’m definitely going to hold on. While it is bad news that the DOJ is recommending that Google be forced to sell Chrome, it’s not written in stone, and there’s a small likelihood of it actually happening.

Here are several aspects to consider.

The Chrome divestiture is not devastating: Chrome, if divested could be valued at an estimated $20Bn, according to Bloomberg Intelligence, about 1% of Alphabet’s market cap of $2Tr, so it’s relatively less harmful.

All Roads Lead To Google Search: Even if the spinoff did happen, that doesn’t mean users would ditch Google’s search engine for rivals such as Bing and Safari, which account for less than 15% of the overall market.

The judge is unlikely to take up the recommendation: There is also the possibility the breakup doesn’t happen. Judge Amit Mehta, who will address Google’s illegal monopolization, could follow precedent.

“I think it’s unlikely because Judge Mehta is a very by-the-book kind of judge, and while breakups are a possible remedy under the antitrust laws, they have been generally disfavored over the last 40 years,” said Rebecca Haw Allensworth, a professor and associate dean for research at Vanderbilt Law School, in an email Monday. “He is very interested in following precedent, as was clear from his merits opinion in August, and the most relevant precedent here is Microsoft.”

The chances of an appeal are very strong: In June 2000, a judge ordered the breakup of Microsoft but that decision was later reversed on appeal. Google has stated that would appeal vigorously.

One of the analysts I follow had a fair point about some of Google’s “predatory or abusive” tactics on their ad-tech platforms, for which there are guidelines/rules that can be enforced for specific violations. But to get into a “European” mindset about regulating companies just because they have strong competitive advantages/moats is completely wrong, in my opinion. If Google didn’t pay Apple $20Bn to be its default search engine, Apple users would still prefer Google Search to Safari or Bing – this was in the court documents. Penalizing them (Google) is a massive overreach.

Google built this from scratch with tons of human and financial capital, at a time when there were several larger search engines in a fledgling, growing internet. The iPhone explosion came later. I would be very surprised if the government succeeds in destroying Alphabet.

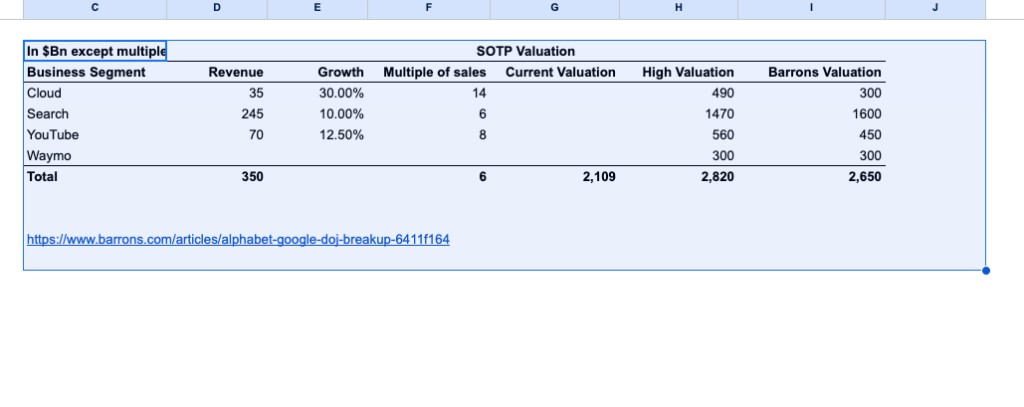

Here is a sum of the parts valuation, which based on these estimates gives Google a higher valuation than its current market cap of $2.1Tr

Hyperscaler Capex Shows Strong Demand For Nvidia’s (NVDA) GPUs.

I know there is excitement in the markets as Nvidia reports Q3-FY2025 earnings after the market on Wednesday 11/20. Nvidia earnings watch parties have become part of the Zeitgeist, and its quarterly earnings are one of the most closely watched events each quarter.

I, however, don’t believe in quarterly gyrations and have been a long-term investor in Nvidia since 2017, having recommended it more than two years ago and then in March 2023 and again in May 2023 as part of an industry article on auto-tech.

I believe the Blackwell ramp is going strong, and reports regarding rack heating issues are just noise in a program of this size.

Capex from hyperscalers will continue to fuel demand for Nvidia’s GPUs in the next year and beyond and even though it’s expensive it remains a great long-term investment.

Capex from hyperscalers – Nvidia’s biggest customers.

AI spending from the hyperscalers is expected to increase to $225Bn in 2024. Cumulatively in the first 9 months of the year, the key hyperscalers who are Nvidia’s biggest clients, have already spent $170Bn, on Capex — 56% higher than the previous year. Here are the estimates for the full year 2024,

Amazon (AMZN) $75Bn

Alphabet (GOOG) $50Bn

Meta (META) $38Bn to $40Bn

Microsoft (MSFT) $60Bn

On their earnings call, hyperscalers’ management committed to continued Capex spending in 2025, but not at the same pace of over 50% seen in 2024.

When quizzed by analysts, hyperscalers also talked about AI revenues, which though are still relatively small compared to the amount of Capex spent, it is growing and growing within their products. Amazon mentioned that its AI business through AWS is at a multibillion-dollar revenue run rate growing in triple-digits year, while Microsoft’s CEO stated that its AI business is on track to surpass $10 billion in annual revenue run rate in Q2-FY2025.

Meta and Alphabet had more indirect inferences about AI revenues. For example, Meta believes that its AI tools improve conversion rates for its advertisers, which creates more demand. On the consumer side, Meta believes that their AI has led to more time spent on Facebook and Instagram. Similarly, Alphabet also spoke about Gemini improving the user experience and its use of AI in search. Seven of the company’s major products—with more than two billion users—have incorporated Google’s AI Gemini model, While Capex from hyperscalers also goes towards infrastructure, and building, which take longer to show good returns, a fairly large chunk goes towards GPUs, which bodes well for Nvidia, which controls more than 80% of the AI-GPU market.

Besides Capex, I also believe in AI and there are several areas where AI has already shown promise.

Code Generation

The low-hanging fruit is being plucked: A quarter of new code at companies like Google is now initially generated by AI and then reviewed by staff. Similarly, GitLabs and GitHub, are providing Dev-Op teams similar offerings.

Other enterprise software companies see huge upsides in selecting a large-language model and fine-tuning the model with their own unique data applied to their own product needs.

I recommended Duolingo (DUOL) for the same reasons, their own AI strengths better their language app, creating a virtuous flywheel of data generation from their own users to create an even better product – data that exists within Duolingo, which is more powerful and useful than a generic ChatGPT product.

Using AI for medical breakthroughs

Pharmaceutical giants like Bristol Myers are using AI for drug discovery at a pace that was impossible before AI and LLMs became available. These are computational problems that need powerful GPUs to research, compute, and process for clinical trials.

Who is the indispensable, ubiquitous, and default option to turn their dreams into reality? – Nvidia and its revolutionary Blackwell GPUs – the GB200 NVL72 AI system, which incorporates 72 GPUs, linked together inside one server rack differentiating Nvidia from its lesser lights like AMD and Broadcom, which at a run rate of $5.5Bn and $11Bn, respectively are minnows compared to the $130Bn behemoth with 80% of that revenue from AI/Datacenter GPUs.

I believe we are in the first innings of AI and Nvidia will continue to lead the way. I continue to buy Nvidia on declines.

Even with the post-earnings bump, which has taken it to $113, I still think it would be worth buying once the euphoria settles. This company is firing on all cylinders and should continue growing for the next 3-5 years.

Shopify excelled on several metrics for the third quarter ended Sep 30th, 2024:

Gross merchandise volume rose 24% to $69.72 billion, beating the consensus estimate of $67.78 billion.

Its revenue rose 26% YoY to $2.16 billion, beating expectations by $50Mn, which was the sixth consecutive quarter of greater than 25% revenue growth for the e-commerce company, excluding logistics.

Monthly recurring revenue rose 28% to $175 million vs. the consensus estimate of $173.6 million. Monthly recurring revenue is a higher-margin subscription revenue business used by larger clients for more features and modules and multi-channel operations. This is Shopify’s growth catalyst for the future, and they’re focused on building and scaling this to differentiate from competitors.

Operating income was up 132% to $283 million, and free cash flow grew 53% to $421 million.

“We have grown free cash flow margin sequentially each quarter this year, consistent with what we delivered last year. These results demonstrate the durability of our business, our multiple avenues for growth, and continued discipline of balancing both future growth investment and operational leverage,” highlighted CFO Jeff Hoffmeister.

The biggest reason behind the 25% jump is the guidance and improving profitability, confirming my earlier thesis that Shopify’s strong focus on providing a rich, multi-channel platform is allowing it to gain market share from plain vanilla, single-feature vendors. Shopify’s management had cited client wins from SalesForce (CRM) earlier as testimonials of its progress.

Guidance

Looking ahead, Shopify sees Q4 revenue growing at a mid-to-high-twenties percentage rate on a year-over-year basis, which is a higher implied rate than the implied guidance. The earlier guidance was 23% so that is quite a large improvement.

Operating Profit Margin will continue to improve, as operating expense as a percentage of revenues decreases to 32% to 33% from an earlier average of 35%.

Free cash flow margin to be similar to Q4 2023 — Around 19.5%, another solid improvement from the previous year.

I plan to buy on declines and hold for the long term of 3-5 years.

Klaviyo beat earnings and revenue estimates for Q3-24, handily, but it wasn’t enough for the market, which punished the stock 12-15% after hours.

I would think that the short interest of 11% also had something to do with the fall, as I don’t believe that the stock is priced to perfection or that earnings “disappointed” investors. Klaviyo had been on a tear, rising from $22, at its low in August 2024, and the 80% rise to $40 needed a breather/correction to consolidate before it resumed rising again; The excellent progress in this quarter confirms the longer-term growth trajectory, and the high-quality business model of the company. I believe it is worth buying on declines, and I bought more at $33 this morning,

Sep 24 quarter results: Adjusted EPS beat by 4 cents or 40% coming in at 14 cents against the 10 cents forecast, and revenue of $235Mn beat by $8Mn or 4%.

Guidance for the next quarter and full year was also raised from the earlier estimate provided. Klaviyo now expects total revenues of $925Mn V $914 at the midpoint and an adjusted operating income of $105, in line with the earlier forecast of $107. Perhaps the market was expecting more here, but this lower operating income is because of an adjustment for higher cash compensation instead of shares, which will be charged in Q4, and going forward accrued in each quarter.

Management also mentioned that 2025 growth would decelerate slightly from Q3-24 growth of 28%, which is fine, consensus analysts’ estimates have pegged the next year’s growth at 24%, so it is likely that Klaviyo will outperform those estimates. Some of the lower growth projections can also be attributed to 2024 revenues coming higher at $924 than the earlier forecast of $895Mn — the growth projected is on a higher base.

I smoothened analysts’ estimates over 3 years from 2024 to 2026, I still get an annual estimated revenue growth of 27%. Klaviyo is valued at 9.5X 2025 sales. This is a P/S to Growth ratio of 0.35, (9.5/27%), which is relatively moderate. I get antsy when it goes above 0.4, and growth drops a lot. Clearly, that’s not anticipated in Klaviyo’s case. What’s remarkable is that an enterprise software company still grew over 30% in the SMB (Small and Medium Business) category.

Here are some Wall Street ratings.

“Klaviyo reported another solid sales quarter against a macro continuing to drive a soft sales environment that has been offset by strong up-market sales execution,” Needham analyst Scott Berg wrote in a note to clients. “Revenue outperformance of 3.9% was at the midpoint of its post-IPO results over the last five quarters. We expect modest share weakness after the company implements a new comp strategy, shifting some [stock-based compensation] to cash comp that will drive 4Q operating margins lower due to a catch-up accrual. We expect investors will ultimately like this change, as our math suggests it could drive somewhere around 8%-10% less annual share dilution.”

Berg kept his Buy rating on Klaviyo but upped his price target to $46 from $40.

Loop Capital analyst Yun Kim also upped his price target slightly, moving to $45 from $40, as he pointed out the results and its view of the business are “somewhat contrary to increasing signs of a weakening environment (especially for a marketing automation vendor).”

Morgan Stanley analyst Elizabeth Porter also upped her price target slightly, moving to $38 from $32, as she said the 34% revenue growth seen in the third quarter puts Klaviyo in “rare air amongst software vendors.”

I added more Lyft, Inc. (LYFT) shares this morning at $17.50 following their excellent Q3-2024 results. I had first recommended Lyft last month at $13.50

Lyft demonstrated remarkable growth in the third quarter of 2024, posting significant gains in operational metrics and financial performance. The rideshare giant reported record-breaking numbers in active riders and total rides, while substantially improving its financial position through increased revenue and robust cash flow generation.

These are its major strengths

Excellent revenue, EBITDA, and Cash Flow growth

Gross Bookings: Reached $4.1 billion, marking a 16% year-over-year increase

Revenue: Hit $1.5 billion, showing substantial growth of 32% year-over-year

Net Loss: Posted $(12.4) million, including a $36.4 million restructuring charge

Adjusted EBITDA: Achieved $107.3 million, up from $92.0 million in Q3’23

Free Cash Flow: Generated $242.8 million, a significant improvement from $(30.0) million in Q3’23

Solid Operational Achievements

The company set new records in its core operational metrics:

Reached 24.4 million Active Riders (9% YoY growth)

Delivered 217 million Rides (16% YoY growth)

Maintained strong driver engagement with record driver hours

Strategic Initiatives In Autonomous Vehicles

Lyft announced significant partnerships in the autonomous vehicle space, positioning itself for future growth:

Formed alliances with Mobileye, May Mobility, and Nexar

Plans to launch autonomous vehicle service in Atlanta by 2025

Strategic Partnership with DoorDash

Established collaboration with DoorDash, the leading U.S. local delivery platform

Introduced exclusive benefits for DashPass members using Lyft services

Lyft has several weaknesses and challenges too.

Secondary player to Uber (UBER) in the rideshare market, with only a 30% market share compared to Uber’s 70%.

Doesn’t have the secondary revenue stream of Uber Eats to absorb fixed costs

Smaller market share and geographic footprint

Limited brand recognition internationally

Heavy reliance on incentives to attract/retain drivers and riders

High customer acquisition costs

Competitive pressure on pricing

Wall Street seems to like it as well

“We think the strong after-hours move is deserved,” Sanderson adds, and think the results will ease concern about Lyft’s ability to grow profitably. “But management’s 15% multi-year [gross bookings] target will still be a debate, as will the company’s position for autonomous vehicles.”

“Efficiencies are driving EBITDA ahead of expectations, and the profitability of the rides business model shined, even through increased investment into rider/demand-based incentives,” Morgan Stanley’s Nowak added, raising his FY25/26 adjusted EBITDA estimates by 9% and 2%, respectively, contributing to a higher price target of $18 from $16, previously.

BofA Securities also lifted its price target, now at $19, as the company has “seemingly limited incremental share losses, focusing on core customers and commuters that are still growing order frequency.”

“We have a Buy rating on Lyft as tailwinds from mobility/transportation recovery in urban areas are outweighing risk factors like driver wage inflation, inflation’s impact on consumer travel, and competition risk from Uber and new autonomous entrants,” BofA’s Michael McGovern and Justin Post said in their research note.

Conclusion – Continuing to accumulate for 3-5 years.

Lyft has a long way to go, but the first and second quarters of adjusted operating profits in a row and strong cash flow generation suggest that it is a serious competitor to Uber.

I had recommended and started buying Lyft in October at around $13-$14, calling it an attractive GARP (Growth At A Reasonable Price), and a very reasonable valuation compared to Uber, which is unlikely to have a monopoly in the ride-sharing market.

Lyft deserves a seat at the table and with excellent Q3 results and raised guidance it looks even more compelling. Sure, there was a massive bump from $14 to $17. post earnings but the valuation is still attractive at 1.1x sales for 12-15% sales growth and at 17x earnings for a 15-17% grower.

Post earnings the stock was up 9% to $188, yesterday, but has given up most of its gains, today. I’m continuing to accumulate.

I’ve owned Qualcomm for a while now, and recommended it in July 2024, and earlier in September 2023, when I wrote a lengthy article on the auto-tech industry. I believe in its long-term strengths and plan to keep the investment for the next three to five years.

Key Strengths include:

The Crown Jewel – Its licensing business with its treasure trove of patents generating 70% margins.

Strong growth from autos – one of the market leaders with Nvidia and Mobile Eye.

Within QCT, Auto was the best performer – sales jumped 68% to $899M. This was the biggest surprise as Qualcomm’s auto sales growth cadence is in the mid-thirties. Auto sales tend to be lumpy so this was a really big positive.

Revenue from handsets rose 12% year-over-year to $6.096B. Handsets tend to struggle sometimes – based on Apple’s fortunes and after drops in the previous year, this was a welcome return to growth.

Its IoT segment has been a slow grower – usually mid-single digits, but it grew 22% this quarter to $1.683Bn.

Licensing revenue rose 21% year-over-year to $1.521B. Licensing is its most lucrative segment with gross margins over 70% – pretty much its crown jewel.

Q1FY2025 Guidance:

Revenue of $10.5B-$11.3B vs $10.61B consensus. At the midpoint, that’s an increase of 3% Non-GAAP diluted EPS of $2.85-$3.05 vs $2.87 consensus, which at the midpoint is also an increase of 3%. from handsets rose 12% year-over-year to $6.096B.

The CEO, Cristiano Anon, had this to say about the quarter

“We are pleased to conclude the fiscal year with strong results in the fourth quarter, delivering greater than 30% year-over-year growth in EPS,” “We are excited about our recent product announcements at Snapdragon Summit and Embedded World, as they continue to extend our technology leadership and position us well across Handsets, PC, Automotive and Industrial IoT. We look forward to providing an update on our growth and diversification initiatives at our Investor Day on November 19.”

Analysts from UBS and J.P. Morgan upped their price targets, while Barclays analyst Tom O’Malley (who kept his Overweight rating and $200 price target) pointed out that there is now a “bifurcation in Android between the high and low end” and Qualcomm is benefiting both in units and average selling price.

At $180, Qualcomm is very reasonably priced at 16x next year’s estimated earnings and 4x next year’s forecasted sales.

Given its market leadership in auto-tech, AI PCs, and sustainable, and recurring high-margin licensing business, Qualcomm should be priced between 20-22x earnings. It spends a good 25% of its revenues on R&D, which will enable it to continue innovating and growing. Even after that, it still returned $1.6Bn to shareholders with $0.7Bn in share buybacks and $0.9Bn in dividends.

But hats off for an amazing quarter, Applovin’s Q3 GAAP EPS of $1.25 beats by $0.32 – This looks like some serious sandbagging.

Revenue of $1.2B (+38.8% Y/Y) beats by $70M. We forget that AppLovin is a $5Bn revenue company, and with these growth rates in a competitive Ad-Tech market, it is seriously behaving like a $1Bn start-up!

What is AppLovin’s secret sauce?: It introduced the new version of its AI-backed ad mediation platform AXON in q1-2023, and the results have been astounding since then. Advertising mediation platforms depend on the strength of the black box that matches targeted customers with relevant ads in real-time, with the best return on investment for the advertiser. It isn’t called performance marketing without reason. You’re only as good as the value that you executed immediately for the publisher or advertiser, which is vastly different from brand building. Clearly AXON has performed for its advertising clients, and this quarter’s outperformance was proof that AXON is the real deal.

From the CEO’s letter to shareholders:

“Our AXON models continue to improve through self-learning and, more importantly, this quarter, from technology enhancements by our engineering team. As we continue to improve our models our advertising partners are able to successfully spend at a greater scale. We’re proud to be a catalyst for reinvigorating growth in our industry.”

In Q3, AppLovin had these amazing metrics:

Revenue of $1.20 billion 39% YoY growth

Net income of $434 million 300% YoY growth at a net margin of 36%

Adjusted EBITDA of $722 million (+72% YoY) at an Adjusted EBITDA margin of 60%.

Net cash from operating activities of $551 million (+177% YoY)

Free Cash Flow of $545 million (+182% YoY).

Financial Guidance Summary 4Q – 24

Total Revenue $1,240 to $1,260 million – Previously $1,180 – At the midpoint that’s a very impressive upward revision of 6%.

Adjusted EBITDA $740 to $760 million

Adjusted EBITDA Margin 60%

AppLovin is sharing this wealth with its shareholders having bought back a total of 5.0 million shares for a total cost of $437Mn, last quarter. The board also authorized an incremental $2.0 billion for buybacks, increasing the total aggregate remaining authorization to $2.3 billion.