The likelihood of only two Fed rate cuts in 2025 sent the markets tumbling yesterday, even as Chair Powell was still answering pointed questions about the resilience of the economy and where inflation was headed in 2025. The S&P 500 eventually closed 2.96% lower. shattering the post-election rally.

The markets had been ignoring the 10-year yield for far too long. The 10-year went from 3.6% in September when the Fed started cutting to 4.40% before the FOMC meeting, signaling that inflation wasn’t completely done and that stock valuations were getting frothy. It unraveled yesterday. Analysts are talking about the 10-year possibly reaching 5%, which will remain bad for stock multiples. The S&P 500 and the Nasdaq Comp are down 4.5% from their highs. Let’s see how the PCE report is on Friday.

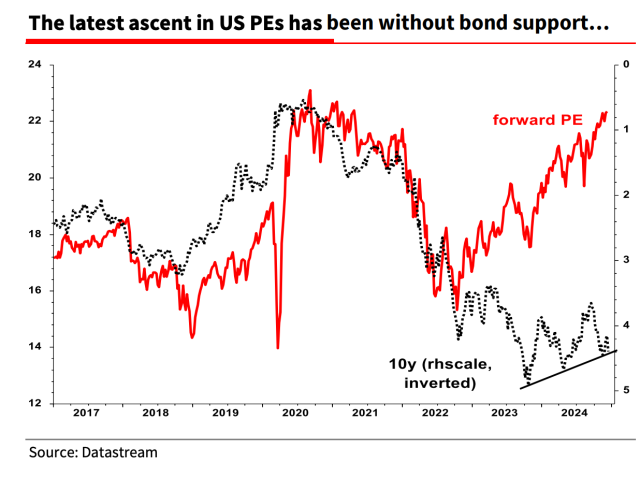

The last time the S&P 500’s P/E ratio was 22, it was 2021, and the 10-year treasury yield was 1%! We are at 4.5% and climbing! The expectations of 4 cuts in 2025 had kept the markets hopeful that the 10-year would follow suit and head back below 4%. Clearly, that’s not happening. Either the index has to come down or the 10-year has to drop to justify these valuations….

Also don’t forget the Fed’s reluctance to cut big for forecast more cuts in 2025 was based on the Sep, Oct and Nov inflation readings, they’ve not even talked about the possible inflationary impact of tariffs and larger fiscal deficits – somebody has to fund the government when they’re not collecting enough taxes, and the weaknesses in the past two treasury auctions suggest that lenders are demanding better rates to lend to the government.