S&P 500 5,022 down 243 points, 4.6% from its all-time high of 5,265.

10-Year US Treasury 4.6%, possibly breaching its Oct 2023 high of 4.98%

There has been a lot of consternation regarding the market in the last two weeks, with the index dropping almost 5% and the 10-year jumping from 4.25 to a high of 4.67% because of the fear of higher for longer interest rates due to stubborn inflation and the reluctance of the Fed to cut rates till they put the inflation genie back in the bottle for good.

Let’s look at it chronologically from Oct 2023.

In late October 2023, when the 10-year was close to breaching 5% Janet Yellen signaled lower interest rates by borrowing $76Bn less than anticipated for the last quarter of 2023. A nod to the nasty run-up in rates, which if unfettered could have been harmful to the economy. The Feds had stopped raising interest rates after the last quarter-point raise in July, and by October, the consensus viewpoint was developing that the markets had done the Fed’s work with the 10-year treasury circling 5%.

Around the same time, multiple Fed officials had said rising Treasury yields are indicative that financial conditions are tightening, possibly making additional rate hikes unnecessary, when the 10-year Treasury yield topped 4.9% on Wednesday, a first since 2007. During this run-up in interest rates, the S&P 500 had dropped to 4,120 from its July high of 4,560.

Once the 10-year treasury topped out, and Q3 2023 earnings season also exceeded expectations it set up the S&P 500 for a furious run up from the October low of 4,120 to about 4,800 by Dec 2023. A massive gain of almost 700 points or about 17%! helped by the Dec dot plot indicating possibly 3 cuts in 2024

We had another positive run in Q1, to the all-time high of 5,265 – both on AI-related earnings and expectations of the 3 cuts materializing in 2024.

My takeaways

- A drop of 4.6% compared to the rise from 4,120 in October to 5,265 (28%) is an overdue correction, not a reason to panic.

- The earnings yield of the S&P 500 = $245/5,022 = 4.9%, which is just above the 10-year treasury yield of 4.6% – we’re getting just 0.3% higher for a riskier investment compared to a risk-free investment of a government security. That’s a very small risk premium, I would think the S&P 500 is likely to fall further to see some semblance of the historic and mean premium of at least 1 to 1.5%.

- The same argument that the Fed used in October is likely to happen as the treasury inches towards 5% –

- a) the market itself has made financial conditions worse, (done the Fed’s work – a 0.6% rise in the treasury is more than 2 quarter-point hikes!)

- b) Buying a risk-free (US Government) long-duration bond paying 5% is a damn good yield and when funds start buying bonds, the yields fall. There will be buyers from all over the world for that kind of yield. Especially in the event of further turmoil in the Middle East – that’s the flight to quality and safety. I don’t see yields topping 5% – I would be shocked if it did.

- The Vix (Volatility Index) or the fear gauge as it is known has shot up to 18-19, after being dormant to steady in the 12 to 14 range through Q1-2024. Computerized trading desks or CTA’s, trade based on volatility which will cause sudden drops and a lot of choppiness, which scares investors. Zero-day options are not helping either. For example, if I see a 1% down day, my first reaction is to lower my buying limits.

- Earnings season should be good, but misses are likely to be hammered disproportionately given the weakness in the market. Semiconductor monopoly ASML, which missed bookings but assured the same full-year guidance and a great 2025, dropped 8% today.

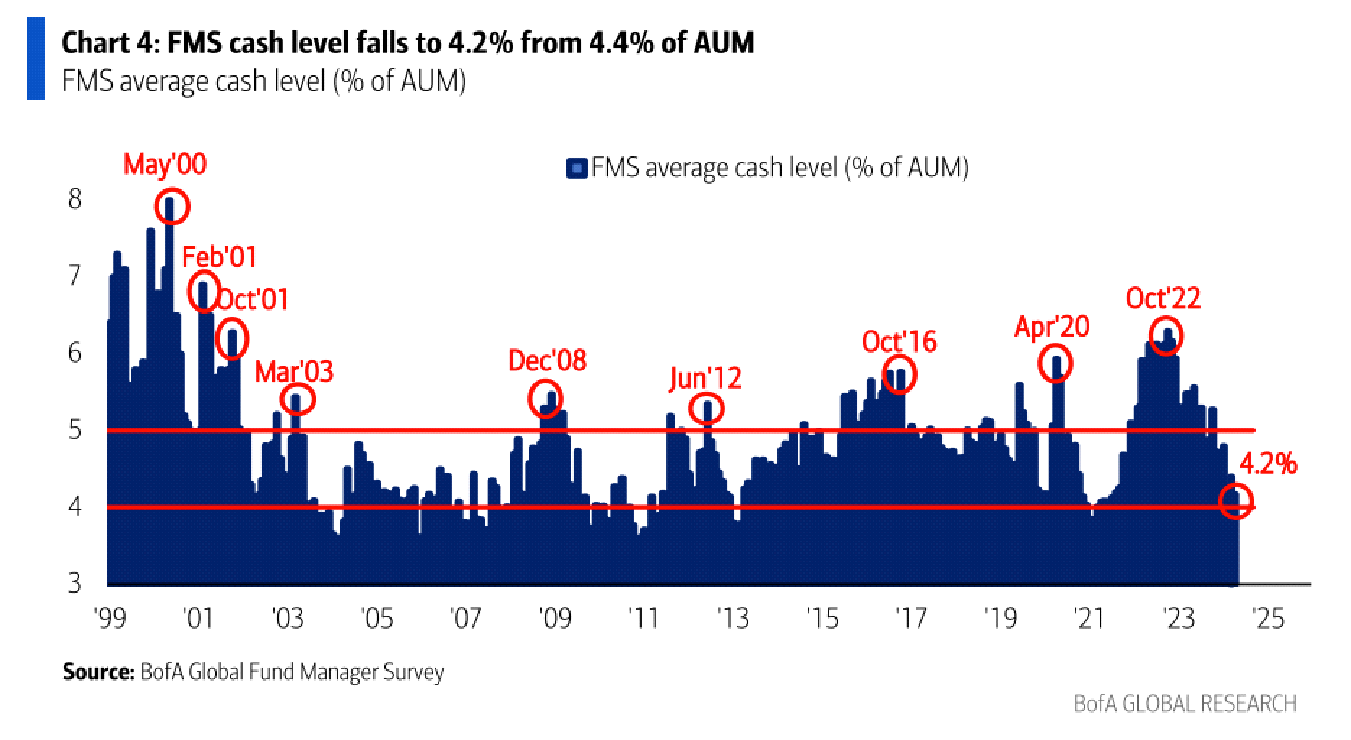

- The graph below is a good contrarian indicator and makes me shake my head at supposedly professional investors. Fund managers have record low cash levels – they’re overextended at only 4.2% cash. When they need the money to pick up bargains, they don’t have it! Some professionals! This won’t help the market recover easily.

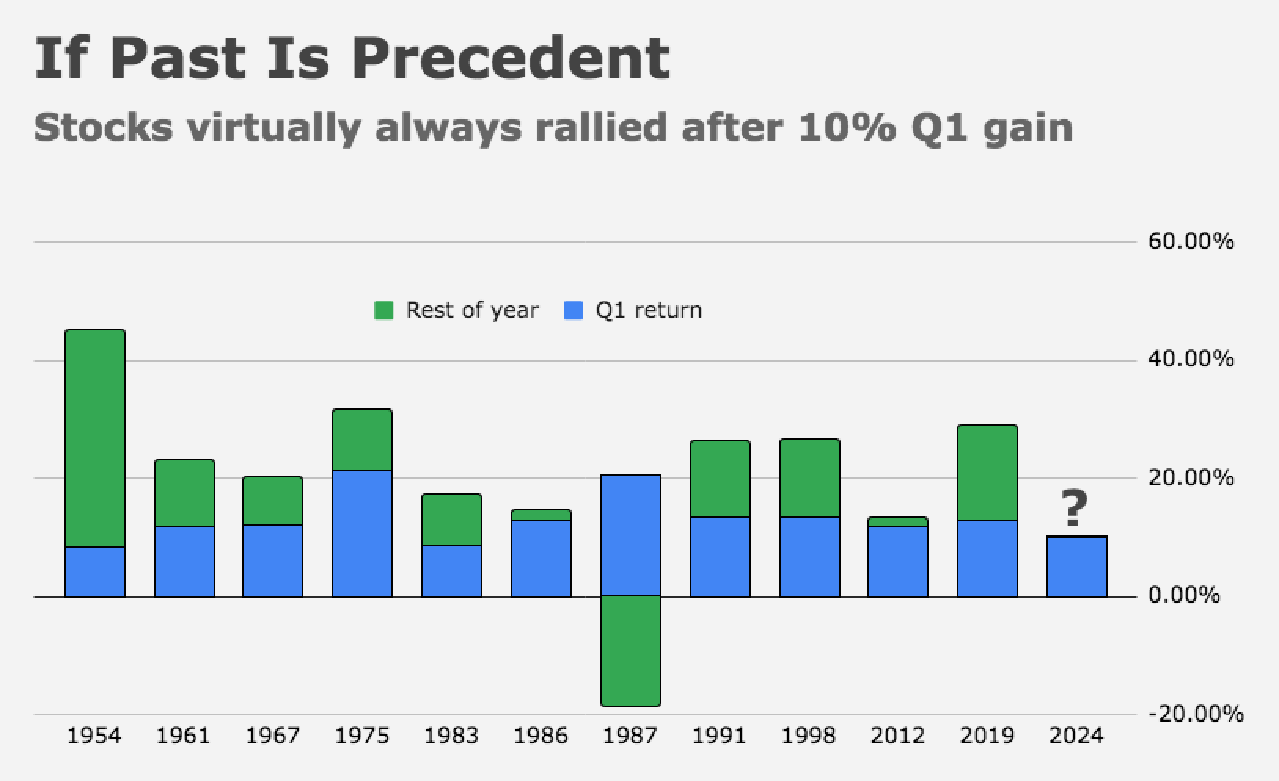

- This is another good chart.

If Q1 has risen more than 10%, on every occasion except 1987 (the year of the Black Monday crash) it has closed the year higher. That doesn’t preclude drawdowns and the average pullback in the years was 11%, with a low of 3%.

- I feel the best way to play this uncertainty is patience and lower limits – the first quarter was exceptional and unlikely to be replicated.

THE LONG-TERM STORY FOR QUALITY STOCKS IS VERY MUCH INTACT, but we would be better off getting good prices. The first to recover will be the high-level quality stocks – see how steady Microsoft is compared to the rest.

- In the last 15 days, my buy trades and recommendations have been limited as you may have noticed and strictly averaging lower with lower limits. I intend to keep it that way.