As expected the Fed cut interest rates by 0.25% bringing the Fed Funds rate to 4.25% to 4.5% To be sure, this is a hawkish cut. The S&P 500 gave up its gains of 0.5% and has dropped 1.5% in a reversal as has the Nasdaq Composite, down a full 2% to 19,703.

The 10-year treasury yield has shot to 4.5%, a harbinger of how the markets believe that the Feds will have to pay more to finance the deficit, with analysts even talking of 5% – a rate seen last October.

The hawkishness stems from the FOMC Median 2025 PCE Inflation Forecast, which rises to 2.5% vs 2.1%

The median forecast of Fed policymakers for the benchmark rate for the end of next year is now 3.9%. That compares with 3.4% back in September. That suggests 50 basis points of easing compared with 100 basis points in September (including the impact of today’s rate cut).

Today’s cut means policymakers have now lowered their benchmark lending rate by a full percentage point since mid-September. The median estimate of Fed officials now sees just two cuts next year. Most folks were expecting three in the forecast.

Fed officials are tipping an unemployment rate of 4.3% next year a shade higher than the current 4.2%. Chair Powell in the conference that followed stressed that he wanted to ensure that labor markets didn’t get derailed when asked about the need to cut.

The Fed’s policy statement also alluded to a slower pace of cuts by saying “the extent and timing” of additional adjustments would depend on the outlook. This too was stressed in the conference that it would always be new data that would matter.

The neutral rate discussed (the rate at which the economy is neither inflationary nor disinflationary) is now 3%, higher than the original 2%, which the Feds were hoping to achieve by 2024, now highly unlikely before 2027.

Given the strength in the economy, with the GDP at 2.8% and projected to grow above 2% next year, a strong labor market with an unemployment rate of only 4.2%, this is not a bad call and regardless of how the market reacted, the caution to cut slower in 2025 is warranted in my opinion.

The main problem is the lack of revenue growth – Starbucks is struggling to grow revenues even 5-7%, same-store sales are declining, it is a saturated market, and with work from home, the big urban markets remain flat or in decline with little chances of recovery, the same for global growth.

Howard Schulz’s bashing of his hand-picked successor is not good for company morale, but he does have a point about improving the customer experience, especially when you keep increasing prices.

Earnings still grow 12-14%, with a multiple of just 18-19, so that’s fairly reasonable, and I don’t see earnings stalling much, they’re an extremely profitable company, with a history of passing price increases. The dividend yield is 3%, which helps.

I would wait for a better price, say mid to high sixties, because even though Starbucks is an absolutely strong and irreplaceable brand, (it would decades for someone to even come close), you’re not likely to see much appreciation – 7-8% per year at the most. In fact, in the last 5 years, the stock was flat, the only way to make a return was to buy it really cheap.

The weaker manufacturing sector is a much smaller part of the economy than services. Manufacturing PMI seems to suggest that economic growth and inflation are not as strong as feared – especially if payroll declines are true to this estimate at least. This is not a major surprise, but the weakness in the service index shows that services is seeing a spillover. This should be watched carefully.

The markets have reacted positively, following yesterday’s bounce back – up ¾ to 1%. (Bad news is good news!)

Tesla reports today, likely to be bad but may be discounted.

Meta reports tomorrow after the market, I’ll put up the preview numbers.

Microsoft and Google report on Thursday.

To round off the week we have the PCE number on Friday, which should give us a better idea of inflation – that is the Fed’s preferred gauge.

U.S. PMI Manufacturing unexpectedly slips into negative territory in April

April PMI Manufacturing Index: 49.9 vs. 52.0 consensus and 51.9 in March. The services PMI did, too, slip to 50.9 (vs. 52.0 expected) from 51.7 a month ago, though it remained in positive territory, with the index still above 50.

The composite PMI (flash estimate) came in at 50.9, down from 52.1 in the previous month, signaling business activity in the U.S. expanded at a slower pace during the month, in the wake of signs of weaker demand.

The group’s measure of employment slid 3.2 points to 48, reflecting shrinking services payrolls and slower growth at manufacturers. The composite index of prices received, meanwhile, pulled back from a 10-month high.

“The more challenging business environment prompted companies to cut payroll numbers at a rate not seen since the global financial crisis if the early pandemic lockdown months are excluded,” Williamson said.

The decline in the employment measure suggests companies see current capacity as sufficient to handle demand. Order backlogs remained in contraction territory during the month.

New business at service providers shrank for the first time since October, with some firms indicating higher borrowing costs and still-elevated prices were limiting demand.

The overall index for services activity decreased to the lowest level in five months, while the manufacturing PMI showed a slight contraction.

“Further pace may be lost in the coming months, as April saw inflows of new business fall for the first time in six months and firms’ future output expectations slipped to a five-month low amid heightened concern about the outlook,” said Chris Williamson, chief business economist at S&P Global Market Intelligence.

S&P 500 5,022 down 243 points, 4.6% from its all-time high of 5,265.

10-Year US Treasury 4.6%, possibly breaching its Oct 2023 high of 4.98%

There has been a lot of consternation regarding the market in the last two weeks, with the index dropping almost 5% and the 10-year jumping from 4.25 to a high of 4.67% because of the fear of higher for longer interest rates due to stubborn inflation and the reluctance of the Fed to cut rates till they put the inflation genie back in the bottle for good.

Let’s look at it chronologically from Oct 2023.

In late October 2023, when the 10-year was close to breaching 5% Janet Yellen signaled lower interest rates by borrowing $76Bn less than anticipated for the last quarter of 2023. A nod to the nasty run-up in rates, which if unfettered could have been harmful to the economy. The Feds had stopped raising interest rates after the last quarter-point raise in July, and by October, the consensus viewpoint was developing that the markets had done the Fed’s work with the 10-year treasury circling 5%.

Around the same time, multiple Fed officials had said rising Treasury yields are indicative that financial conditions are tightening, possibly making additional rate hikes unnecessary, when the 10-year Treasury yield topped 4.9% on Wednesday, a first since 2007. During this run-up in interest rates, the S&P 500 had dropped to 4,120 from its July high of 4,560.

Once the 10-year treasury topped out, and Q3 2023 earnings season also exceeded expectations it set up the S&P 500 for a furious run up from the October low of 4,120 to about 4,800 by Dec 2023. A massive gain of almost 700 points or about 17%! helped by the Dec dot plot indicating possibly 3 cuts in 2024

We had another positive run in Q1, to the all-time high of 5,265 – both on AI-related earnings and expectations of the 3 cuts materializing in 2024.

My takeaways

A drop of 4.6% compared to the rise from 4,120 in October to 5,265 (28%) is an overdue correction, not a reason to panic.

The earnings yield of the S&P 500 = $245/5,022 = 4.9%, which is just above the 10-year treasury yield of 4.6% – we’re getting just 0.3% higher for a riskier investment compared to a risk-free investment of a government security. That’s a very small risk premium, I would think the S&P 500 is likely to fall further to see some semblance of the historic and mean premium of at least 1 to 1.5%.

The same argument that the Fed used in October is likely to happen as the treasury inches towards 5% –

a) the market itself has made financial conditions worse, (done the Fed’s work – a 0.6% rise in the treasury is more than 2 quarter-point hikes!)

b) Buying a risk-free (US Government) long-duration bond paying 5% is a damn good yield and when funds start buying bonds, the yields fall. There will be buyers from all over the world for that kind of yield. Especially in the event of further turmoil in the Middle East – that’s the flight to quality and safety. I don’t see yields topping 5% – I would be shocked if it did.

The Vix (Volatility Index) or the fear gauge as it is known has shot up to 18-19, after being dormant to steady in the 12 to 14 range through Q1-2024. Computerized trading desks or CTA’s, trade based on volatility which will cause sudden drops and a lot of choppiness, which scares investors. Zero-day options are not helping either. For example, if I see a 1% down day, my first reaction is to lower my buying limits.

Earnings season should be good, but misses are likely to be hammered disproportionately given the weakness in the market. Semiconductor monopoly ASML, which missed bookings but assured the same full-year guidance and a great 2025, dropped 8% today.

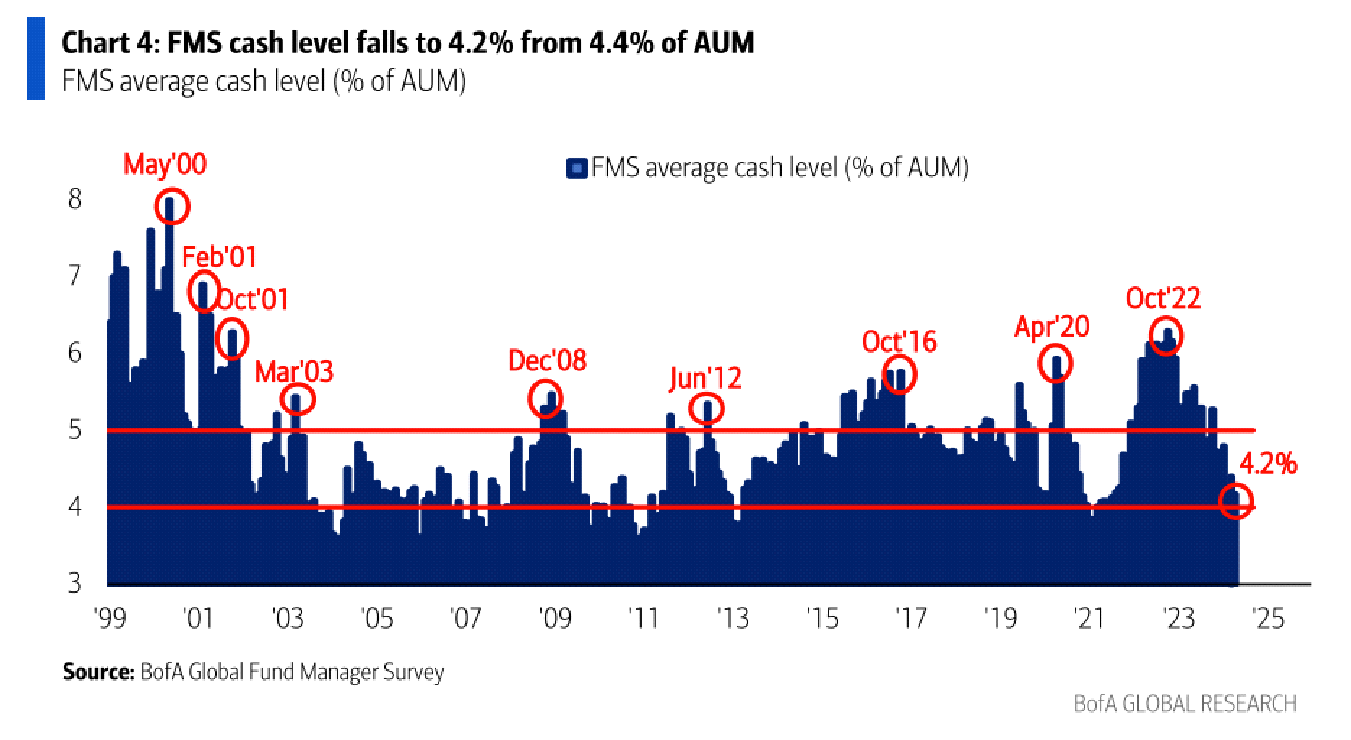

The graph below is a good contrarian indicator and makes me shake my head at supposedly professional investors. Fund managers have record low cash levels – they’re overextended at only 4.2% cash. When they need the money to pick up bargains, they don’t have it! Some professionals! This won’t help the market recover easily.

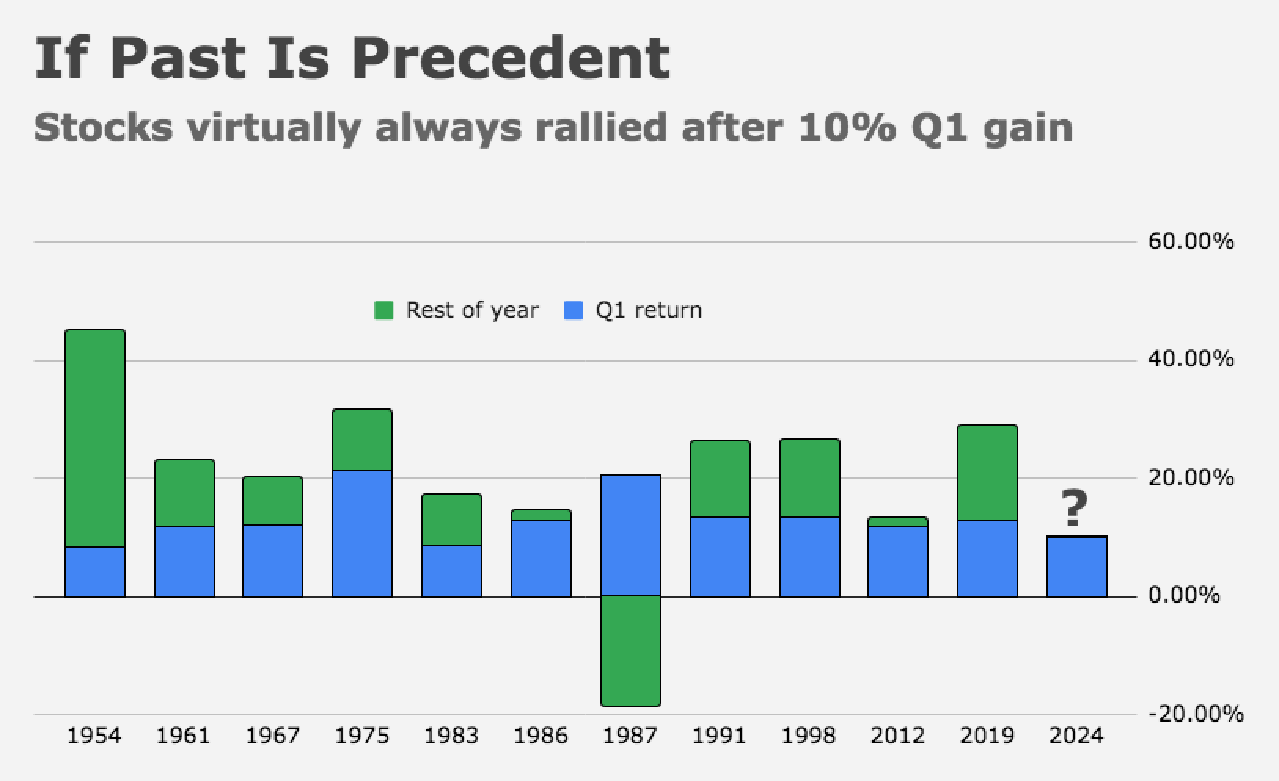

This is another good chart.

If Q1 has risen more than 10%, on every occasion except 1987 (the year of the Black Monday crash) it has closed the year higher. That doesn’t preclude drawdowns and the average pullback in the years was 11%, with a low of 3%.

I feel the best way to play this uncertainty is patience and lower limits – the first quarter was exceptional and unlikely to be replicated.

THE LONG-TERM STORY FOR QUALITY STOCKS IS VERY MUCH INTACT, but we would be better off getting good prices. The first to recover will be the high-level quality stocks – see how steady Microsoft is compared to the rest.

In the last 15 days, my buy trades and recommendations have been limited as you may have noticed and strictly averaging lower with lower limits. I intend to keep it that way.

ASML – Lithography, Monopoly in EUV machines, each machine costs north of $200 Mn, absolutely vital for lower node semis like 3nm, which is powering the latest I-phone among others.

ASML is at the pole position since it’s a critical component for AI and/or high-end chips. Every chip being planned or in production for AI acceleration or incorporating AI acceleration is produced on a 5 nm or smaller node that requires EUV

They also have the lower-end D-EUV machines, which are also successful.

Here’s a good link to the equipment technology market.

Lam Research on the other hand is strong in Etch and Deposition, which is exposed to cyclicality because it’s more of a mass market commodity with competition for AMAT, KLAC, and Tokyo Electronics. But the pickup from customers like Micron, which itself is riding the AI boom for high-grade memory equipment is a big benefit for Lam. To me the biggest strength is the resilience in the last 10 years with an EPS CAGR of 28% – that is a huge deal, cyclicals/commodity producers never get that.

Fed’s preferred inflation gauge subsides, in line with consensus, in February

Core PCE Price Index, which excludes food and energy, rose 0.3% M/M in February vs. +0.3% consensus and 0.5% prior (revised from +0.4%).

On a year-over-year basis, core PCE increased 2.8% Y/Y, compared with the +2.8% consensus and +2.9% prior (revised from 2.8%).

Including food and energy prices, the PCE Price Index grew 0.3% M/M, less than the +0.4% expected and slowing from +0.4% in January (revised from +0.3%).

Prices for goods rose by 0.5%, bolstered by energy prices, and prices for services rose 0.3%. Food prices edged up 0.1%, while energy prices jumped 2.3% during the month.

2.5% Y/Y vs. +2.5% expected and +2.4% prior.

Personal income increased less than expected, up 0.3% M/M vs. +0.4% expected and +1.0% prior, the U.S. Commerce Department said on Friday.

Personal outlays climbed 0.8% M/M, exceeding the +0.5% expected and accelerating from +0.2% in January.

Real disposable income, which is adjusted for inflation, declined 0.1% M/M in February, while real personal consumption expenditures increased 0.4%.