I thought that Chair Powell was impressive at the FOMC March 20th, press conference. He came across as very balanced, cautious, and data-dependent. Clearly, these are not easy with the chaos emanating from the executive branch, and handling an economy that was headed for a soft landing which now may get derailed needs kid gloves.

Chair Powell paid heed to the soft data – forward-looking surveys for inflation and tariffs from sources like the Michigan Consumer Sentiment Index and the PMIs; data that points to softness and uncertainty in the economy borne out of tariffs, deportations, and higher inflation expectations, which all seemed under control just a few months back. He balanced it with what’s showing up as reported, which is nowhere as bad, clearly the surveys are just leading indicators for now.

The Fed’s revised numbers for 2026 are as follows:

Inflation 2.8% from 2.5%

GDP lower at 1.8% from 2%

The Unemployment 4.4% from 4.3%

Given that the softer surveys are not showing up in the reported numbers yet, the proposed strategy is to wait and watch.

When pressed about why he’s going ahead with two rate cuts when clearly inflation is not below the 2% objective, he stressed the Fed’s dual mandate of full employment – which needs cuts in the face of a weakening economy, and tariff uncertainties.

Similarly, he also stressed that the weaker data wasn’t yet showing up in the job numbers, which meant that they were in no hurry to cut, but were ready and willing to act as required.

I believe the markets heaved a sigh of relief that they haven’t called for more or earlier cuts: I agree with the notion that they’re going to live with higher inflation but not let the economy falter. It is the right way to go. The S&P closed 1.17% higher for the day. At least its moving up from correction territory.

The word transitory came up, a bad penny that’s never left Chair Powell. I understood it as transitory similar to Trump’s first term, in the sense, that they still don’t know the impact. He emphasized that it’s not “transitory” like the mistake they made post-COVID in 2021, and scrambled to raise the rates in 2022. That seems fair.

The bottom line – a lot of ponderables, and moving parts. Clearly, we’ve got our work cut out to make money in 2025! Many have never seen a stagflationary environment and to be sure it is going to be tough navigating it.

In the shorter term, I would expect the S&P 500 to rise a bit more, there is the 200DMA hovering at 5,705, which is a key resistance level – hopefully, we clear that before the PCE next week.

I sold 15-25% of several stocks on Friday, 02/21/2025 as a de-risking exercise in the wake of weakening economic indicators, which I wrote about in this article.

Here’s the list and you can see them in the Trade Alerts Section as well.

ARISTA NETWORKS (ANET) $101

ADVANTEST CORP SPON ADR (ATEYY) $63

AMAZON INC (AMZN) $218

APPLIED MATERIALS INC COM (AMAT) $174

APPLOVIN CORP COM CL A (APP) $430

ARM HOLDINGS PLC (ARM) $147

BROADCOM INC COM (AVGO) $222

DOORDASH (DASH) $201.65

DUOLINGO INC CL A COM (DUOL) $410

DUTCH BROS INC CL A (BROS) $80

GITLAB INC CLASS A-COM (GTLB) $65.75

KLAVIYO INC (KVYO) $42.75

MICRON TECHNOLOGY INC (MU) $101

NETFLIX (NFLX) $1,012

SAMSARA INC (IOT) $54.25

SPOTIFY TECHNOLOGY S.A. COM (SPOT) $626

Earnings alone won’t save this market from a correction

Earnings season for Q4-2024 is mostly over except for Nvidia (NVDA), which reports on 02/26. M-7, and overall earnings were mostly lackluster and while most beat sandbagged estimates as always, the beats were nothing to write home about.

Instead, there was a lot of pressure for Q4 earnings to outperform to trump bearish indicators such as stubborn inflation, high valuations, tariff uncertainty, the likelihood of no interest cuts in 2025, difficult housing markets with 7% mortgage rates, weakening consumer sentiment, and so on….

Analysts, according to FactSet are still forecasting an estimated $268-$275 in 2025 S&P 500 earnings (about 11.5% growth), but this number seems more and more likely to either come in at the lower end or be revised lower as the year progresses. Second – the two-year back-to-back gains of 23% are a historical anomaly so I have to keep that in mind of a likely down year or a flat to 7-8% gain from already high levels.

Against all that is the $320Bn in Capex from the hyperscalers (That’s real money, not an economic survey or estimate – therefore the strongest catalyst ), which is extremely good for the AI industry and a very strong and vocal belief in the fundamentals – longer term we are on solid footing, and the AI story is just beginning, there are a lot of benefits to reap.

Active Risk Manangment

In short – a balancing act, which means there has to be active risk management. And especially when almost all the economic indicators came worse than expected, with sticky inflation and slower growth – stagflation. The Michigan survey of inflation expectations is followed closely by the Feds, and the weakening PMIs coincide with Walmart’s lower guidance. The reports have a lot of meat and don’t paint a pretty picture.

I’m not selling/trading the index or the stalwarts like Apple (AAPL), and Alphabet (GOOG) – there will be a flight to quality, thus not recommended. Even with a correction I don’t see the S&P 500 falling beyond 5,600-5,780. 5,780 was the Nov 5th election day level, that’s just 3.8% lower, not worth it.

My portfolio is tech-centric, and sometimes the drops in those are between 20% and 30% – AppLovin (APP), Palantir (PLTR), and Duolingo (DUOL) are examples, plus they’ve performed far better than expectations so taking some off is a great de-risking strategy for me.

There has been a spate of economic indicators in the past week or so, which are bearish for the market indicating a possible correction or at the very least a level of caution.

Let’s take a look.

The PMI – The Purchasing Manager’s Index – a 17 Month Low!

The index fell to a 17-month low at 50.4 in February, down from 52.7 in January, indicating that activity had slowed to a virtual standstill. Worse, cost inflation accelerated even with the lower activity, and was absorbed by suppliers who were unable to pass it on – indicating a possible stagflationary spiral.

Economists didn’t see it coming with expectations of 53.

It also marked the slowest pace of business expansion since September 2023, driven by a renewed contraction in services output that partially offset faster manufacturing growth. New order growth weakened significantly, while employment edged lower amid rising uncertainty and cost concerns.On the price front, input cost inflation accelerated to its highest level since last September, while selling prices saw their slowest increase in three months. Finally, business optimism about the coming year slumped to its lowest since December 2022, except for last September, amid concerns over federal government policies related to domestic spending cuts and tariffs, as well as worries over higher prices, and broader geopolitical developments.

The University of Michigan’s consumer sentiment index fell to 64.7 in February from 71.7 in January. Economists polled by FactSet were expecting a much better 67.5.

Year-ahead inflation expectations rose to 4.3% from 3.3% in January. This is a worrying sign, high inflation expectations hurt the mass consumer and spending.

Tariffs are scaring consumers as all five index components weakened this month, with durables lower by 19% mostly on ears that tariff-induced price increases were imminent.

Year-ahead inflation expectations jumped up from 3.3% last month to 4.3% this month, the highest reading since November 2023 and marking two consecutive months of unusually large increases.

Current Conditions Index: 65.7 vs. 68.7 expected and 75.1 January.

Consumer Expectations Index: 64.0 vs. 67.3 consensus and 69.5 prior.

Existing home sales of 4.08Mn also came in below expectations at 4.11Mn.. Economists surveyed by The Wall Street Journal had estimated a monthly decrease of 2.6%. In 2024, home sales fell to the lowest level since 1995 for the second straight year.

First-time home buyers seemed to be priced out by the double whammy of higher prices and high mortgage rates. I had reported earlier that the brave home buyers from 2022-2024 would feel the pinch of not getting to re-finance their 6-7% mortgage and clearly, few takers are willing to take that risk now.

Cash is at a record low:

According to the BOFA Global Fund Manager survey, cash is at 3.5% – the lowest level since 2010!

That begs the obvious question? With only 3.5% cash what’s left to buy the dip? With over-ownership of the M-7, these stocks aren’t just overbought, a) There’s previous little cash left to buy when the prices get attractive and b) You already own all of them, where’s the room to add more?

We could be in a fading, twilight of a bull run and headed for a correction according to Scott Rubner, managing director for global markets and tactical specialist at Goldman Sachs.

Rubner was categorical in stating the good times from corporate buybacks, retail investors jumping in on every dip, 401k inflows, and beginning of the year investing was waning, and once the corporate buyback period went into the quiet period for Q2, fund flows would move away from equities.

According to Rubner:

“My highest conviction is that this massive ability to buy dip alpha is starting to wane.” Rubner also said that hedge funds have allocated a lot of risk back into the market. Global equities saw the largest net buying in two months last week.

Rubner backed his findings with two key statistics; His assessment that computerized trading desks selling triggers, in the event of a market dip would unload $62Bn worth of equities compared to just $9.55Bn of buying on buying signals – pretty asymmetric towards the downside. Secondly, he also cited “A net retail buy imbalance for the last 22 days, including the top three largest days on record, he said. “This cohort is happy to buy any 2-3% dips for now.”

Q4-24 Earnings weren’t good enough:

The FactSet report on S&P 500 Earnings on 02/14 was just average and for this market to keep rising average won’t do – the valuations The M-7, bellwethers were also sluggish and will have a hard time taking the indices higher.

And while I’m positive about AI, semiconductors, and several fundamentally strong tech companies, valuations have been stretched for a while, thus it would be prudent to take advantage of some of the prices by booking profits, which I have started and posted in the trade alerts section.

While a set of economic indicators doesn’t necessarily doom the market, the downside surprise indicates that we’re not paying enough attention to economic weaknesses, against a backdrop of stretched valuations and interest rates that refuse to fall. The correct de-risking strategy would be to sell and keep cash available for better bargains.

I’ve owned it for over two years but will pyramid (add smaller quantities on a large base) it further.

Why is this company still worth investing in after a 20% post-earning bump?

Four important catalysts

Databricks partnership: The partnership with Databricka, which is much better known and valued increases brand awareness and opens a lot of new opportunities and doors.

This could accelerate growth from the current 22-23%.

Strong customer base: 90% of its revenues are coming from 100K + ARR clients.

The $1Mn+cohort saw the highest growth, and Confluent managed a net ARR of 117%, indicating strong upselling.

A changing data processing market: The entire batch processing model could be up for grabs – customers moving at the speed of light and willing to pay for the latest technology could be a huge TAM.

This is a paradigm shift, which Confluent has been trying to build into for a decade. 2025 might be that inflection year, with all the AI build-outs and use cases that are likely to need live processing – Confluent is the leader in that field. To be sure it’s not going to throw data processing models into obsolescence, why would you spend money on data that doesn’t need to be processed in real-time, but could take a large chunk of that market?

Snowflake acquiring RedPanda: Snowflake is reportedly trying to buy streaming competitor RedPanda for about 40x sales: While it’s not an obvious comparison, Red Panda is supposedly less than 10% of Confluent’s revenues but growing at 200-300%. But it’s the synergy with the larger data provider that’s getting it a massive price tag – Snowflake would love to have this arrow in its quiver of data tools.

Confluent is best positioned to take advantage of the possible shift from batch processing to processing in data streaming; its founders invented Apache Kafka, the open-source model for data streaming. And while its own invention is available for free – managing and maintaining it at scale needs the paid version. Over the years with the focus on Confluent Cloud, Confluent gets 90% of its $1Bn revenue from customers over $100K in annual revenue.

Confluent has the cash the tech chops and the focus – sure Apache Kafka is open source and many cloud service providers like AWS and Microsoft also provide enough competition, but no one has the product breadth that Confluent does.

I would not be surprised if Confluent’s multiple expands from the current 8x sales after this earnings call.

Here are the details of the December 2024, 4th quarter earnings:

Q4 Non-GAAP EPS of $0.09 beat by $0.03.

Revenue of $261.2Mn (+22.5% Y/Y) beat by $4.32Mn.

Q4 subscription revenue of $251Mn up 24% YoY

Confluent Cloud revenue of $138Mn up 38% YoY

2024 subscription revenue of $922Mn up 26% YoY

Confluent Cloud revenue of $492Mn up 41%YoY

1,381 customers with $100,000 or greater in ARR, up 12% YoY.

194 customers with $1Mn or greater in ARR, 23% YoY.

Stubborn inflation and the fear of inflationary policies such as tariffs, budget deficits, and deportations had led to high 10-year treasury yields jumping to 4.8% before dropping to 4.66% today.

This, in turn, has spooked the S&P 500, which gave up its entire post-election bounce before bouncing back today.

The S&P 500’s current yield of 4.6% is less attractive compared to the 10-year treasury yield of 4.66%, questioning the risk-reward balance.

However, while the 4.66% yield will compete for investors’ funds, patient investors who can stomach a correction should do much better scooping up high-quality bargains.

There are enough positives to come from the new administration, such as lower taxes, less regulation, and business-friendly policies, which will trump the negative of high interest rates.

Will 10-year treasury yields of 4.66% drag down the market?

The equity risk premium

The current yield for the S&P 500 (NYSEARCA:SPY) is 4.6% or the 2025 Consensus Bottoms Up EPS of $274/S&P 500 of 5,953 = 4.6%. Comparatively, the 10-year treasury yield stands at 4.66% The commonsense argument is that if the US treasury gives me a risk-free return of 4.66% why should I make a risky equity index investment, yielding even less at 4.6%?

Risk-averse and conservative investors usually require a risk premium to invest in equities. During the great deflationary period from 2009, after the Great Financial Crisis, to Feb. 2020 (pre-pandemic), the equity premium was quite large as shown below. The average yield premium was 2.79%, and it rarely fell below 2%. The 10-year yield averaged 2.43%.

Source:Fountainhead, Yahoo Finance

In an inflationary environment, with the 10-year at 4.66%, we’re getting a discount of 6 basis points or 0.06%, which begs the question

a) Either I should get a premium return for that risk or

b) I should pay less to increase my yield.

Stubborn inflation

With stubborn inflation, a reduction in yields looks unlikely, and many would patiently wait for the reduction in the index to get in at a decent price. Not surprisingly, as of Jan. 14th, we’ve given back almost all the Trump bump, falling to 5,800, a mere 0.5% from the Nov 5th election date close of 5,782, which has now bounced back to 5,953 following the better-than-expected CPI report.

Last September, I was confident that the Fed’s reduction of 0.5% would lead to a 10-year closing between 3.25% and 3.5% in 2025. At an earnings yield of 4.6%, that would have been a fairly decent premium of around 1.25%. Initially, it did drop to 3.6%; however, given sticky inflation readings in the next 3 months and a stronger-than-expected job market and economy, 10-year yields have gone the opposite way climbing to 4.79%, before dropping to 4.66% — leading to the Feds anticipating just two cuts in 2025 in their dot plot from the December 18th FOMC meeting. Four weeks later, the markets have taken a step further, anticipating just a paltry 27 basis points reduction in 2025.

This morning, on Jan. 15th, the CPI report was much better than expected, with core CPI coming in only 0.2% higher from a month earlier, – a drop after increasing 0.3% in each of the previous four months. Its YoY increase was only 3.2%, lower than 3.3% in November and below the 3.3% consensus.

The 10-year yield dropped to 4.66% – a huge 13 basis point drop, leading to a 1.7% increase in the S&P 500 by mid-afternoon to 5,5953.

The Fed’s December meeting minutes also revealed a Fed that was worried about higher inflation from the incoming administration’s tax and tariff policies, which contributed to their forecast of only 2 cuts in 2025. From the FOMC minutes:

Almost all participants judged that upside risks to the inflation outlook had increased.

The S&P 500 (SP500) dropped 1% on January 7th, when PMI data revealed persistent price increases on the services front. It dropped another 1.5% with the massive 256,000 gain in net new jobs created, with the non-farm payrolls released on January 10th. Price action in the treasury clearly confirms this worry and, given how fast traders have sold bonds, suggests that this could well continue. Market headlines blaming the weakness in stocks on bond yields have only increased. Simply, the markets are sanguine until they’re not, and then the dam breaks.

The incoming administration’s volatility premium

I also believe that traders are assigning a “volatility” or even a “drama” premium if you will. Markets hate uncertainty. If you’re a bond manager already facing three years out of the last four of losses, witnessing the bizarre behavior of our elected officials towards the end of the year of getting a simple budget extension is going to weigh on your decisions. Why buy the treasury at 4.79% when the yield could shoot through 5.5% if there is more drama getting anything done in Washington with a razor-thin majority and an executive branch executing through Twitter?

An emboldened Trump, with a penchant for implausible actions such as annexing Greenland and the Panama Canal, will only increase bond market jitters.

High interest rates hurt Main Street, not just the market

The other factor that worries me about rising interest rates is the higher interest burden on other sectors such as commercial real estate lending, and residential mortgages. Residential mortgage rates are over 7% now, and while over 92% of residential mortgages are at much lower fixed rates, I would think that a significant amount of home purchases (some of which were chasing high-priced homes in short supply due to inventory shortages) have been made at higher mortgage rates in the last two-three years with the hope that they could refinance at cheaper rates – and clearly that hasn’t happened in 2023, and 2024 and from the looks of it, very unlikely to happen in 2025.

According to Trepp estimates, roughly $1.7 trillion, or nearly 30% of outstanding debt, is expected to mature from 2024 to 2026. This is commonly referred to as the “maturity wall.” CRE debt relies heavily on refinancing; therefore, most of this debt is going to need to be repriced during this time.

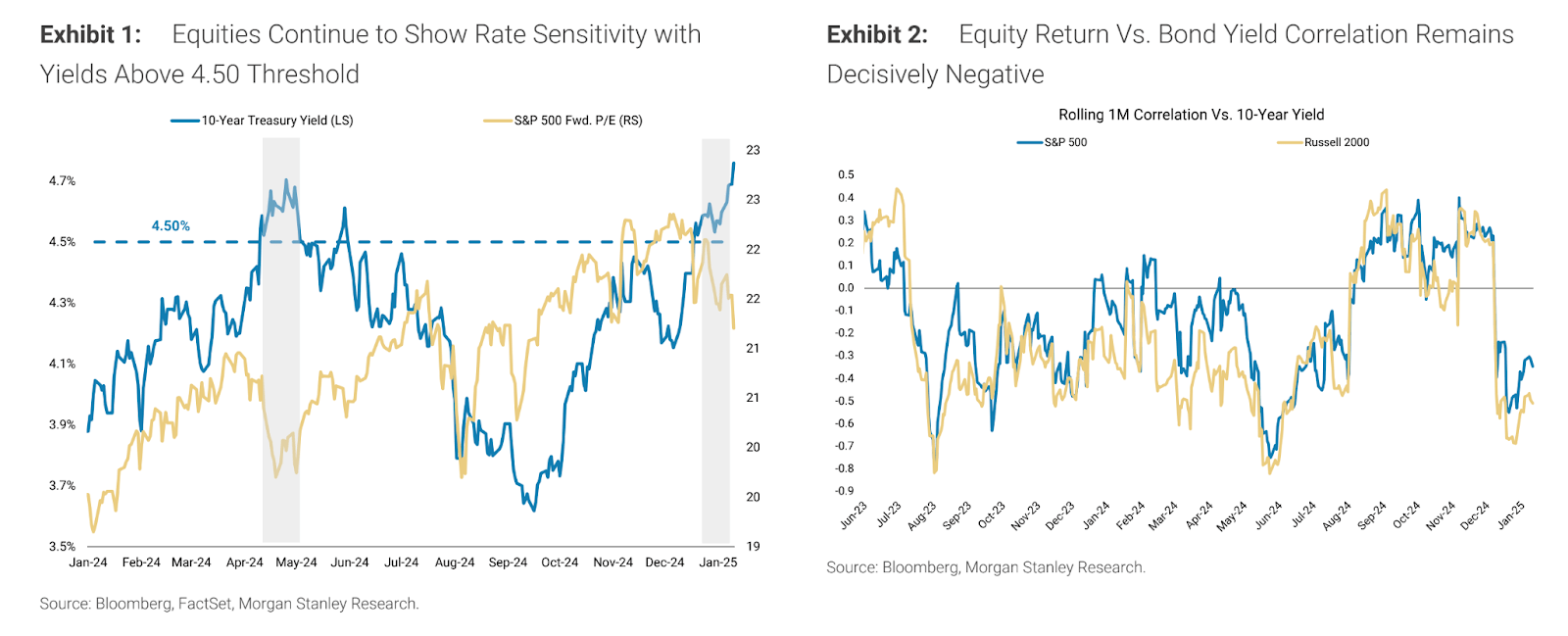

The 4.5% yield threshold

Source: The 4.5% yield threshold (Bloomberg, FactSet, Morgan Stanley Research, The Heisenberg Report)

Last April the S&P 500 P/E fell in tandem with the 10-year rise, and it currently looks to be following the same path, not auguring well for the market in 2025.

Could we get “Trussed”?

UK 10-year bond yields surged by 30 basis points on January 8th, to 4.925%, bringing back bad memories of the harrowing 49 days of Elizabeth Truss’s short-lived premiership in 2022.

Back then, Truss had made the mistake of unveiling an unfunded budget of 45Bn GBP of tax cuts when inflation rates were about 11%! UK Equity, Bond, and Currency markets sank, with many even suggesting that the UK government’s treasury was no better than that of a Third World country. Almost destroying a weak Gilt market ultimately led to her resignation.

Fast-forward to 2025 – the 30 basis point drop to a level not seen since 2008 has 2 repercussions. 1) Bond markets are reacting very strongly to governments not having enough control over their country’s inflation. Punishment was swift and severe. It was the 4th day of drops in the UK bond market.

2) The second repercussion, and what worries me; is this going to happen in the US market as well as the incoming administration starts working on their planned tariff hikes, which will increase inflation; if so, where does the yield stop?

Tax cuts can be inflationary

Trump’s proposed tax cuts reduce tax revenues and increase deficits, which is inflationary.

The incoming administration plans to extend the 2017 tax reductions, reduce the corporate tax rate, and decrease or eliminate taxes on certain types of income. Here is the analysis from taxfoundation.org:

Using the Tax Foundation’s General Equilibrium Model, we estimate Trump’s tax proposals would increase long-run GDP by 0.8 percent, the capital stock by 1.7 percent, wages by 0.8 percent, and employment by 597,000 full-time equivalent jobs.”

“We estimate the proposals would increase the 10-year budget deficit by $3 trillion conventionally and $2.5 trillion dynamically. The debt-to-GDP ratio would increase from its long-run projected level of 201.2 percent to 223.1 percent on a conventional basis and 217 percent on a dynamic basis. Increased deficits and a higher debt load would require higher interest payments on the debt that would reduce American incomes as measured by GNP by almost 0.8 percent; the higher interest payments drive a wedge between the long-run effect on output of 0.8 percent and the long-run effect on GNP of -0.1 percent.

As you can see above, the repercussions can be good for the economy with higher GDP, but it will also be inflationary and expensive to service with higher interest rates. What’s also significant is that the administration believes that they can make up the shortfall by increasing tariffs, which in my opinion will worsen an already high inflation rate.

What the bulls say: There are a lot of positive factors as well

Juxtaposed with the negativity of high interest rates are the positive effects of excellent earnings growth from the S&P 500, lower taxes, and less regulation.

Source: S&P 500 Earnings (FactSet)

FactSet’s estimates call for a strong 14.64% growth in the S&P 500 for 2025 to 274.19, followed by 13.6% growth to 311.44 in 2025. In the years that I’ve been using FactSet, I’ve seen that the variation is not significant for the index. I strongly believe that the S&P 500 earnings would come in between 267 and 281, with an error margin of just 2.5%. But the problem is not in the performance – it’s the valuation, we’re priced to perfection as seen below, and disappointments could be the main catalyst for a drop.

Source: S&P 500 P/E Ratios (The Heisenberg Report, Datastream)

The last time the S&P 500 P/E was above 20, the 10-year was around 2%, currently, we’re at a P/E of over 21.73, but the 10-year is at 4.66%.

Good earnings and cash flow over the last few years have led to low debts on several investment grade and lower balance sheets. The level of fallen angels – or companies below investment grade, is at its lowest level in 25 years.

Risk premiums are not mandatory for equity investments

The lack of an equity risk premium is not the end of the world and as we can see from the chart below, in higher interest rate environments from 1985 to 2000, there never was one. The biggest premiums have been in the deflationary era, post the GFC from 2009 before the Fed started raising interest rates to quell inflation.

A high interest rate doesn’t kill the equity market just because of a lack of a risk premium, but it provides competing offerings at much lower risk, and we saw that hurt the equity market in 2022 when the Fed started raising interest rates aggressively to contain inflation. I, myself, put money in high-yield CDs and corporate bonds through 2023.

A 5% Treasury yield should attract buyers

I believe there could be a lot of buying if the treasury breaches 5%. In October 2023, when the Middle East conflict was raging, bond yields briefly touched 5% from where they reversed very steeply, on buying and a subtle push from Treasury Secretary Janet Yellen, who reduced the size of government auctions by $76Bn. Will history be repeated? I think it’s likely that there will be substantial buying of 5% treasury bonds, as do several analysts, and money managers.

Inflation: The worst is likely behind us

The PPI came in a little lower than expected at 0.2% M/M in December 2024, versus a consensus of +0.4% and November’s reading of +0.4%. Even better, the core PPI was flat M/M, significantly lower than the expected rise of 0.3%. The benign numbers triggered a relief rally on Jan. 14th, and the CPI report which came in today (Jan 15th, 2025), did even better with the core CPI beating estimates, leading to a drop of 13 basis points in the 10-year and a huge 1.7% gain in the S&P 500. This could be the beginning of a trend reversal.

Positive effects of lower taxes

Even as we move towards a more inflationary environment with unfunded tax cuts, the Tax Foundation believes that lower taxes would increase long-run GDP by 0.8 percent, capital stock by 1.7 percent, wages by 0.8 percent, and employment by 597,000 full-time equivalent jobs.

Rekindled animal spirits are great for Main Street

Small businesses, which are major employers and contributors to US GDP, are very optimistic about the Trump administration’s policies, which should augur well for the economy. Small businesses are notably excited about higher sales, less regulation, increased chances of finding high-quality labor, stabilizing inflation or price increases, and importantly, better credit conditions due to less regulation. Not surprisingly, the groups’ uncertainty indicator has dropped as well.

What is the best way forward to invest in a difficult year?

Keep realistic expectations

There are enough bullish and bearish factors without either one having a clear edge. In 2023, the S&P had a reasonable P/E of around 18, allowing the big AI bang from Nvidia’s May earnings report, to propel the index to a 24% gain. In 2024, the S&P 500 gained 23% as the AI trend continued, but now inflation has persisted and the S&P trades at an expensive 21.7 times 2025 forward earnings. The chances of a third year of 20% gains are rare; it’s happened only 3 times in the past 100 years, but two of those were in 1935, and 1936 following the great depression, and then the third one in the nineties during the dot-com bubble. So, my expectations have to be very realistic.

Wait for bargains

The correction should continue, which allows us to scoop up bargains: In my opinion, we’re likely to see 5,500 before 6,500 in 2025. The S&P had wiped out the post-election bump, dropping to 5,800, past the 20 and 50 DMAs, before reversing this morning. Should it drop again, I expect strong support around its 200 DMA of 5,582.

Besides, I think this market will continue to correct until interest rates stabilize, which won’t happen until we see a drop in PCE readings (due at the end of January) wage growth, and a reduction in volatility, which is high with the VIX hovering between 17 and 19. There’s also precious little one can do about volatility; this is a Presidential stock-in-trade. The first few weeks of the Trump administration should be fairly volatile, as they roll out their tariff, deportation, and tax plans. The incoming President has stated that they intend to get off the ground very quickly with executive orders on day one, with immigration a big priority, which means we should get a fairly good view of deportations and their inflationary effects. The Trump administration also showed in their previous innings, firing unrealistic salvos as opening bids – and thus I assume a zero chance of 60% tariffs – the realistic number is likely to be much lower, but the drama will unsettle the market.

Focus on the big picture and stick to the fundamentals

To me, the biggest investment factor is always the fundamentals of great companies, which trumps macro, economic, or technical factors in the long run, unless they’ve historically deviated from the norm, and we’re not anywhere close to that. The stellar jobs report for December confirms how strong the economy is, in fact, higher wages are your biggest defense against inflation – good news is good news. It’s idiotic to hope that the labor market weakens, so the Fed can cut rates – very twisted logic, which hopes for weakness in the economy!

Earnings

Earnings will continue to do well, as we saw from FactSet’s estimates and especially across the M-7; No matter how much we complain about the lack of breadth, the M-7 will still carry the economy and the markets. The M-7 are not outliers, they are truly entrenched in the economy and are in the rare, sweet spot of being secular and sustainable growers and stalwarts with strong brands, pricing power, and huge moats.

Stocks to buy on declines

Taiwan Semiconductor Manufacturing Company Limited (TSM) – I first recommended TSMC in August 2023, and continue to add on declines. Its December monthly revenue grew 58% YoY and fourth quarter revenue grew 39% YoY, suggesting a strong beat of its mid-point guidance, and confirming its strength as one of the strongest pillars of the semiconductor industry.

NVIDIA Corporation (NVDA) – The CES showcased a strong Nvidia with its foray into the PC market, its new gaming chips, and the introduction of Cosmos, which takes its Ominverse segment to much higher levels with the addition of Blackwell architecture. Any short-term thinking about Blackwell delivery delays is just noise and a great opportunity. I’ve started buying around $132 and will continue to add on declines. I’ve owned Nvidia for a long time and have recommended it in March 2023, and July 2023.

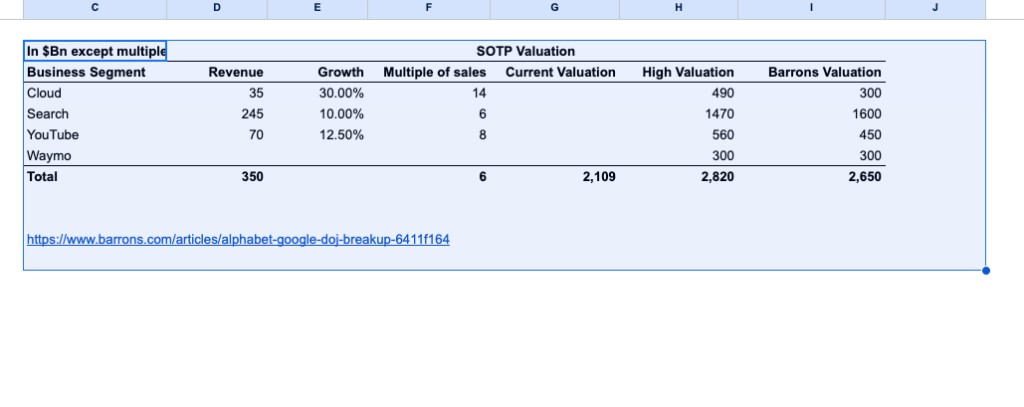

Alphabet Inc. (GOOG) (GOOGL) does not get enough recognition for its market leadership and moats in Search, YouTube, Google Cloud, and Waymo, with far too much focus on the antitrust ruling. Given the new administration’s anti-regulatory stance, I don’t believe Alphabet will be hurt as badly, and even in the worst case, here’s a sum of the parts valuation, which at $2.6Tr is higher than its current market value of $2.35Tr.

I would also add the following on declines: Duolingo, Inc. (DUOL), the market leader in language learning and a huge beneficiary of AI, Marvell Technology, Inc. (MRVL), which has a strong position in ASICs and is very attractive at 12 times sales growing at 40%, and 41 times earnings growing at 33%,

Corrections are healthy for the market, and I look forward to buying on declines.

Turnarounds rarely succeed. Ask Warren Buffet, who tried his best to turn around textiles major Berkshire Hathaway, which was suffering from a barrage of cheaper imports (sound familiar?) before giving up and turning it into the holding company and investment giant that is today. Rolls-Royce (RYCEY) is in the midst of one in the cutthroat world of aerospace engineering and manufacturing and is having a banner year with its stock up 82% to date.

Can it continue or sink under its three difficult cyclical segments, aerospace, defense, and power with low margins and tough competition? –

A year and a half ago, CEO Tufan Erginbilgic took over a struggling company with pandemic-induced challenges, operational inefficiencies, and persistent financial setbacks. His approach was bold and uncompromising: radical cost-cutting, operational streamlining, and a laser-focused strategy to transform Rolls-Royce’s fundamental business model. He did admirably, trimming the workforce by 6% and reducing expenses by £400 million. He also raised prices, optimized procurement processes, and renegotiated contracts.

As a result, in the first 6 months of 2024, Rolls-Royce did an excellent job with

19% revenue growth to £8.18Bn

74% increase in operating profit to £1.2Bn, with an OPM of 14%

Free cash flow improvement by 225% to £1.2Bn

Net debt reduced to its lowest level in five years to £822 million

The turnaround was led by Civil Aerospace (its largest division), and the strongest performer with 27% revenue growth, which benefited from post-pandemic air travel recovery. What’s more, its higher-margin service revenues also grew 27% to 68% of division sales, indicating a robust and recurring revenue stream. The aerospace segment benefited from strong growth in in-flight hours for engines under long-term service agreements, and large engine deliveries to OEMs increased by 4% with overall OEM deliveries up 26%.

Besides the volume growth, Rolls-Royce also passed on elevated costs, after successfully renegotiating long-term service agreements. Airbus, which saw increased demand for the Trent engines and General Dynamics for its Gulfstream engines, as big customers helped; Competitor General Electric saw its equipment sales fall year-on-year in the second quarter due to lower LEAP engine deliveries.

Defense and Power Systems also showed growth. Defense revenues grew 18%, with strong submarine platform sales and higher service revenue. Power Systems saw a smaller 6% revenue increase, mainly from Datacenters, a segment that certainly holds greater promise.

What does the future look like and can they continue with the turnaround?

Aerospace: Rolls-Royce exclusively provides the engines for the Airbus A350 and A330neo and those airplanes have seen some solid sales momentum which will drive value for the company. The services division will provide better margins

Defense: Given the stronger Republican emphasis on defense, I believe Rolls Royce should see better impetus from defense budgets in the next 4 years.

Power: Data center power needs should be a great opportunity for Rolls-Royce especially with the small modular reactor. The UK government has already picked Rolls-Royce as one of four sources, as has the Czech electricity company, CEZ.

Key Risks:

Execution challenges: This is not their first trip out of the despair well, and once the benefits from cost-cutting dissipate, they still have to grow.

Exposure to global air travel trends, which will slow down after the post-COVID revenge travel boom. Regional revenues were lower and didn’t participate in the post-COVID travel boom.

The company is worth buying: I plan to buy Rolls Royce on declines after such a large run-up for the following reasons.

Reasonable valuation for a GARP (Growth At A Reasonable Price): Analyst consensus estimates call for revenue growth of 8-10% for the next three years at a paltry P/S valuation of just 2.4x sales. Rolls-Royce is also slated to grow EPS by 20% in the next three and has a reasonable P/E of 26, or just 1.3.

Improving margins: Given the improvements in operating margins and the focus on efficiency, margins could improve further and help earnings grow.

Diversification: The company’s diversified portfolio – civil aerospace, defense, and power systems – helps hedge against sector-specific cyclicality.

Datacenter Opportunity: I also believe that Datacenter requirements for power will be a big winner for Rolls-Royce.

Dividends: They’re also reinstating dividends at 30% of after-tax profits, which should provide a floor for the stock price.

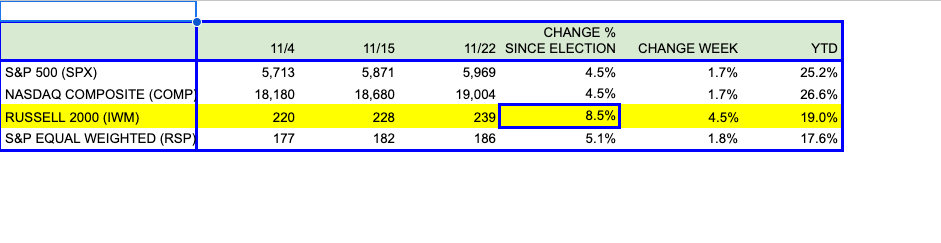

The Russell 2000 (IWM) ETF and the S&P 500 Equal Weighted Index have been outperforming the S&P 500 and the NASDAQ Composite since the election. Last week was no exception.

The IWM comprises 2,000 of the smallest capitalized companies in the market.

The IWM has gained 8.5% compared to the S&P 500’s and the Nasdaq Composite’s 4.5% gain since Nov 4th, 2024, and 4.5% in the last week, significantly higher than the 1.7% each gained by its larger counterparts.

Last week, breadth was better across the board. The NYSE Advance/Decline Ratio or $ADRN, finished on Friday 11/22 at 3.6, (3.6 stocks advancing V 1 decline), it averaged 2.29 for the past week, and 1.81 since the Nov 5th election against an average of 1.61 for the Year To Date.

Clearly, everyone wants in and has been wanting in since the election – money has shifted from chasing the M-7 and other large caps to a larger pool of small-cap stocks. The markets have aggressively seized that opportunity and have bid them faster than the large caps. Is the breadth a bullish sign or is the euphoria unsettling?

Let’s look at some of the main reasons:

Business-Friendly Populist Government: To some extent, there is a perception that small caps are closer to the economy than the M-7, and other tech behemoths, which explains why the prospects of tax cuts, pro-business policies,and less regulation would improve their fortunes much more than the large caps.

Small Caps are cheaper: Large-cap tech is also perceived to be much more expensive – the average earnings multiples are lower for small caps.

Everybody and their uncle owns Nvidia: Investors and traders are likely overexposed to big-tech stocks and need to diversify, but were afraid to do so. A Bank of America study found “Long M-7” the most crowded trade in the markets just two weeks back.

Animal spirits are up: More risk-taking, Hell the markets are likely to go up with the pro-market Trump administration and I should add. Consumer sentiment seems to have boomed since the election.

FOMO – The small caps are up and I don’t have exposure, I need to jump on this train.

Should we remain invested or does breadth call for caution?

Business-Friendly Populist Government: I agreewith the tax cuts and deregulation, but we need to see if the proposed tariff plans could derail this.

Small Caps are cheaper: Small caps may be cheaper, but if you take out the premium that should go to secular growers with sustainable competitive advantages, and look at the risks associated with smaller, struggling businesses, the difference is not that stark, and sometimes it’s the opposite. Some businesses are just terrible, with no competitive advantages, and low prospects of growth, and their stock prices are driven purely by momentum. These are risky businesses you don’t want to own, period. For now, I believe this rotation may continue for a few weeks more, but the bottom line — if I’m looking at a small cap or even a small cap index, I’m going to look at the underlying fundamentals before making a call. I’m not riding any gravy trains here.

Everybody and their uncle owns Nvidia: That is true – the overownership is well documented, and when there is overownership, the scope to continue rising is much, much lower. To some extent, the earnings have to catch up with the valuation or the stock will just drift, and you’ll find large-cap investors rotating into small-caps.

Animal spirits are up: Drill, Baby, Drill, DOGE, etc, all sound great during the honeymoon period, but the jury is still out, we’ll have to see how everything works in 2025. I’m on the fence on this, it’s still a show-me story, and the possibilities of this going south are not small.

FOMO: This I am seeing first hand – For example, Navitas (NVTS) one of my weak small-cap picks, which sank from $4 to $1.60, has suddenly bounced back from the dead to $2.40 in a week! I’m not going to look a gift horse in the mouth, I didn’t add but I’m hoping it bounces back to at least where I can exit. Navitas is actually in the right place at the right time – its focus is on power saving for data centers, which could be a huge business, but it’s currently, heavily exposed to China with 57% of sales there, (it is in 60% of all the cell phones in the world). Besides Navitas, several other stocks popped in the previous week, without any changes in fundamentals.

Conclusion

Breadth is good for the market, just not at the expense of the usual due diligence.

All five reasons helped a fundamentally sound, and highly high-quality small-cap stock like Confluent, (CFLT) a favorite, that I’ve owned and written about. It’s a $1Bn revenue company with an $8Bn market cap, which shot up from $27.50 to $31.50 in the past week for several reasons.

The business-friendly and animal spirits bounce – because now enterprises seem to be spending; The halo effect from Snowflake (SNOW) the 4x larger data warehousing, market leader had a great quarter and guidance last week; Confluent, which serves the same enterprise market with data streaming is also being seen as a beneficiary and now gets the higher multiple.

The over-ownership bounce: I would rather add more Confluent and Klaviyo (KVYO) shares because my portfolio already has high exposure to large caps.

Small Caps could continue to outperform in the near term, just to catch up. As we saw from the chart, on a YTD basis they’re still behind at 19% to 25%.

An interesting article in the Wall Street Journal discusses Google’s anti-trust case in more detail. Quoting from the article:

“Some of the DOJ’s proposals were expected, such as the divestiture of the Chrome browser and a ban on payments to Apple AAPL in exchange for default or preferred placement of Google’s search engine on Apple’s devices”, which are minor and something Google could take in its stride.

But the government’s proposal of “Restoring Competition Through Syndication And Data Access”, could be more harmful in the long run.

Restoring competition through access, which involves Google providing its search index—essentially the massive database it has about all sites on the web—to rivals and potential rivals at a “marginal cost.”, in my opinion, is stripping Google of its IP, and competitive advantages, which it has built through decades of human and monetary capital. It is draconian and a massive overreach. It gets worse, if the government has its way, Google would also have to give those same parties full access to user and advertising data at no charge for 10 years.

For now, it’s a wish list, a starting point of a high ask, which I’m sure the government expects to be whittled down to something less harmful and gives it some bragging rights.

Points to consider

This could harm/scare other tech giants.

The Turney Act makes this government agnostic, it guarantees judicial oversights for antitrust actions.

Alphabet has significant and solid resources and defensible arguments to fight this, mainly the 2 decades of resources put into building this moat.

The stock is likely to stay range-bound or sideways because of the legal issues, where most investors would likely be cautious, even though this morning itself there have been strong buy calls from analysts.

I’m definitely going to hold on. While it is bad news that the DOJ is recommending that Google be forced to sell Chrome, it’s not written in stone, and there’s a small likelihood of it actually happening.

Here are several aspects to consider.

The Chrome divestiture is not devastating: Chrome, if divested could be valued at an estimated $20Bn, according to Bloomberg Intelligence, about 1% of Alphabet’s market cap of $2Tr, so it’s relatively less harmful.

All Roads Lead To Google Search: Even if the spinoff did happen, that doesn’t mean users would ditch Google’s search engine for rivals such as Bing and Safari, which account for less than 15% of the overall market.

The judge is unlikely to take up the recommendation: There is also the possibility the breakup doesn’t happen. Judge Amit Mehta, who will address Google’s illegal monopolization, could follow precedent.

“I think it’s unlikely because Judge Mehta is a very by-the-book kind of judge, and while breakups are a possible remedy under the antitrust laws, they have been generally disfavored over the last 40 years,” said Rebecca Haw Allensworth, a professor and associate dean for research at Vanderbilt Law School, in an email Monday. “He is very interested in following precedent, as was clear from his merits opinion in August, and the most relevant precedent here is Microsoft.”

The chances of an appeal are very strong: In June 2000, a judge ordered the breakup of Microsoft but that decision was later reversed on appeal. Google has stated that would appeal vigorously.

One of the analysts I follow had a fair point about some of Google’s “predatory or abusive” tactics on their ad-tech platforms, for which there are guidelines/rules that can be enforced for specific violations. But to get into a “European” mindset about regulating companies just because they have strong competitive advantages/moats is completely wrong, in my opinion. If Google didn’t pay Apple $20Bn to be its default search engine, Apple users would still prefer Google Search to Safari or Bing – this was in the court documents. Penalizing them (Google) is a massive overreach.

Google built this from scratch with tons of human and financial capital, at a time when there were several larger search engines in a fledgling, growing internet. The iPhone explosion came later. I would be very surprised if the government succeeds in destroying Alphabet.

Here is a sum of the parts valuation, which based on these estimates gives Google a higher valuation than its current market cap of $2.1Tr

Post earnings the stock was up 9% to $188, yesterday, but has given up most of its gains, today. I’m continuing to accumulate.

I’ve owned Qualcomm for a while now, and recommended it in July 2024, and earlier in September 2023, when I wrote a lengthy article on the auto-tech industry. I believe in its long-term strengths and plan to keep the investment for the next three to five years.

Key Strengths include:

The Crown Jewel – Its licensing business with its treasure trove of patents generating 70% margins.

Strong growth from autos – one of the market leaders with Nvidia and Mobile Eye.

Within QCT, Auto was the best performer – sales jumped 68% to $899M. This was the biggest surprise as Qualcomm’s auto sales growth cadence is in the mid-thirties. Auto sales tend to be lumpy so this was a really big positive.

Revenue from handsets rose 12% year-over-year to $6.096B. Handsets tend to struggle sometimes – based on Apple’s fortunes and after drops in the previous year, this was a welcome return to growth.

Its IoT segment has been a slow grower – usually mid-single digits, but it grew 22% this quarter to $1.683Bn.

Licensing revenue rose 21% year-over-year to $1.521B. Licensing is its most lucrative segment with gross margins over 70% – pretty much its crown jewel.

Q1FY2025 Guidance:

Revenue of $10.5B-$11.3B vs $10.61B consensus. At the midpoint, that’s an increase of 3% Non-GAAP diluted EPS of $2.85-$3.05 vs $2.87 consensus, which at the midpoint is also an increase of 3%. from handsets rose 12% year-over-year to $6.096B.

The CEO, Cristiano Anon, had this to say about the quarter

“We are pleased to conclude the fiscal year with strong results in the fourth quarter, delivering greater than 30% year-over-year growth in EPS,” “We are excited about our recent product announcements at Snapdragon Summit and Embedded World, as they continue to extend our technology leadership and position us well across Handsets, PC, Automotive and Industrial IoT. We look forward to providing an update on our growth and diversification initiatives at our Investor Day on November 19.”

Analysts from UBS and J.P. Morgan upped their price targets, while Barclays analyst Tom O’Malley (who kept his Overweight rating and $200 price target) pointed out that there is now a “bifurcation in Android between the high and low end” and Qualcomm is benefiting both in units and average selling price.

At $180, Qualcomm is very reasonably priced at 16x next year’s estimated earnings and 4x next year’s forecasted sales.

Given its market leadership in auto-tech, AI PCs, and sustainable, and recurring high-margin licensing business, Qualcomm should be priced between 20-22x earnings. It spends a good 25% of its revenues on R&D, which will enable it to continue innovating and growing. Even after that, it still returned $1.6Bn to shareholders with $0.7Bn in share buybacks and $0.9Bn in dividends.

I had recommended Alphabet (GOOG) as a great long-term buy between $150 and $170 on several occasions.

Last evening, Google knocked it out of the park with really stellar results. I bought more shares this morning, and am reiterating a Buy.

I believe analysts’ consensus earnings are a bit conservative and Google will continue to beat estimates with better growth and operating margins.

Google’s earnings quality is better than several tech giants for the following reasons.

It has a near monopoly in Search

Market leadership in media with YouTube.

A strong first-mover advantage with Waymo.

A fast-growing Google Cloud business, third only to and catching up with Azure and AWS.

Its earnings and growth are sustainable, thus it deserves a better valuation and multiple.

Let’s take a closer look at Q3 earnings.

Q3 GAAP EPS came in at $2.12 per share, beating expectations of $1.85 per share $0.27, or 14% – This was a substantial beat.

Revenue of $88.3Bn (+14.9% Y/Y) beat by $2.05B or 3%.

Consolidated Alphabet revenues in Q3 2024 increased 15%, or 16% in constant currency, YoY to $88.3Bn reflecting strong momentum across the business.

Google Services revenues increased 13% to $76.5 billion, led by strength across Google Search & other, Google subscriptions, platforms, and YouTube ads.

Total operating income increased 34% and operating margin percent jumped a huge 4.5% to 32%.

Google Cloud revenues grew a whopping 35% to $11.4Bn led by accelerated growth in Google Cloud Platform (GCP) across AI Infrastructure, Generative AI Solutions, and core GCP products, with record operating margins of 17% as the cost per AI query decreased by 90% over the past 18 months.

Cloud titans Amazon (AWS) and Microsoft (Azure) have commanded huge valuations for their cloud computing businesses; with Google Cloud growing at 35%, it should continue to narrow the gap over the next 5 years. Also importantly, AWS and Azure have operating margins over 30%, and should Google continue to scale and leverage their existing fixed costs, they can reach the same margins. I also believe as they get better at AI, they should be able to charge more.

Based on consensus analysts’ estimates Alphabet’s EPS should grow to $11.60 in 2027 from $5.80 in 2023 – that’s an annual growth rate of 18%. Comparatively, Apple‘s estimated EPS growth through FY2027 is slower at 14%, and it sports a P/E of 33 compared to Google’s 22. Alphabet’s P/E is closer to the S&P 500’s P/E of 21!

I believe this is too low, and there is a lot of potential for its stock to appreciate just on the lower valuation.

Besides the strong EPS, a lot of Google’s expenses are noncash depreciation and amortization and their cash flow margins are strong. They generated operating cash of $31Bn on $88Bn last quarter, or a 35% cash flow margin.

The antitrust regulation will remain a possible negative on Alphabet, but the final decision is still years away as Alphabet vigorously appeals the decision.

{kind=link}