I thought that Chair Powell was impressive at the FOMC March 20th, press conference. He came across as very balanced, cautious, and data-dependent. Clearly, these are not easy with the chaos emanating from the executive branch, and handling an economy that was headed for a soft landing which now may get derailed needs kid gloves.

Chair Powell paid heed to the soft data – forward-looking surveys for inflation and tariffs from sources like the Michigan Consumer Sentiment Index and the PMIs; data that points to softness and uncertainty in the economy borne out of tariffs, deportations, and higher inflation expectations, which all seemed under control just a few months back. He balanced it with what’s showing up as reported, which is nowhere as bad, clearly the surveys are just leading indicators for now.

The Fed’s revised numbers for 2026 are as follows:

Inflation 2.8% from 2.5%

GDP lower at 1.8% from 2%

The Unemployment 4.4% from 4.3%

Given that the softer surveys are not showing up in the reported numbers yet, the proposed strategy is to wait and watch.

When pressed about why he’s going ahead with two rate cuts when clearly inflation is not below the 2% objective, he stressed the Fed’s dual mandate of full employment – which needs cuts in the face of a weakening economy, and tariff uncertainties.

Similarly, he also stressed that the weaker data wasn’t yet showing up in the job numbers, which meant that they were in no hurry to cut, but were ready and willing to act as required.

I believe the markets heaved a sigh of relief that they haven’t called for more or earlier cuts: I agree with the notion that they’re going to live with higher inflation but not let the economy falter. It is the right way to go. The S&P closed 1.17% higher for the day. At least its moving up from correction territory.

The word transitory came up, a bad penny that’s never left Chair Powell. I understood it as transitory similar to Trump’s first term, in the sense, that they still don’t know the impact. He emphasized that it’s not “transitory” like the mistake they made post-COVID in 2021, and scrambled to raise the rates in 2022. That seems fair.

The bottom line – a lot of ponderables, and moving parts. Clearly, we’ve got our work cut out to make money in 2025! Many have never seen a stagflationary environment and to be sure it is going to be tough navigating it.

In the shorter term, I would expect the S&P 500 to rise a bit more, there is the 200DMA hovering at 5,705, which is a key resistance level – hopefully, we clear that before the PCE next week.

There has been a spate of economic indicators in the past week or so, which are bearish for the market indicating a possible correction or at the very least a level of caution.

Let’s take a look.

The PMI – The Purchasing Manager’s Index – a 17 Month Low!

The index fell to a 17-month low at 50.4 in February, down from 52.7 in January, indicating that activity had slowed to a virtual standstill. Worse, cost inflation accelerated even with the lower activity, and was absorbed by suppliers who were unable to pass it on – indicating a possible stagflationary spiral.

Economists didn’t see it coming with expectations of 53.

It also marked the slowest pace of business expansion since September 2023, driven by a renewed contraction in services output that partially offset faster manufacturing growth. New order growth weakened significantly, while employment edged lower amid rising uncertainty and cost concerns.On the price front, input cost inflation accelerated to its highest level since last September, while selling prices saw their slowest increase in three months. Finally, business optimism about the coming year slumped to its lowest since December 2022, except for last September, amid concerns over federal government policies related to domestic spending cuts and tariffs, as well as worries over higher prices, and broader geopolitical developments.

The University of Michigan’s consumer sentiment index fell to 64.7 in February from 71.7 in January. Economists polled by FactSet were expecting a much better 67.5.

Year-ahead inflation expectations rose to 4.3% from 3.3% in January. This is a worrying sign, high inflation expectations hurt the mass consumer and spending.

Tariffs are scaring consumers as all five index components weakened this month, with durables lower by 19% mostly on ears that tariff-induced price increases were imminent.

Year-ahead inflation expectations jumped up from 3.3% last month to 4.3% this month, the highest reading since November 2023 and marking two consecutive months of unusually large increases.

Current Conditions Index: 65.7 vs. 68.7 expected and 75.1 January.

Consumer Expectations Index: 64.0 vs. 67.3 consensus and 69.5 prior.

Existing home sales of 4.08Mn also came in below expectations at 4.11Mn.. Economists surveyed by The Wall Street Journal had estimated a monthly decrease of 2.6%. In 2024, home sales fell to the lowest level since 1995 for the second straight year.

First-time home buyers seemed to be priced out by the double whammy of higher prices and high mortgage rates. I had reported earlier that the brave home buyers from 2022-2024 would feel the pinch of not getting to re-finance their 6-7% mortgage and clearly, few takers are willing to take that risk now.

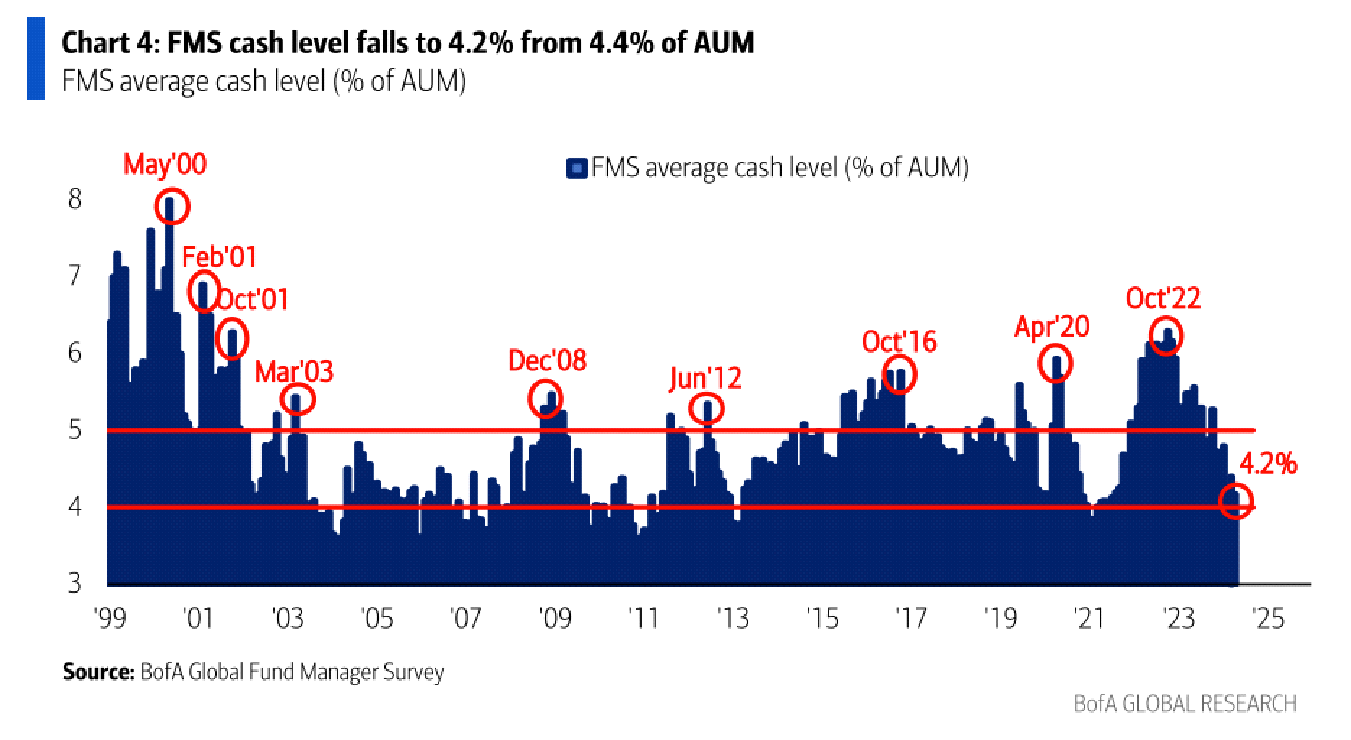

Cash is at a record low:

According to the BOFA Global Fund Manager survey, cash is at 3.5% – the lowest level since 2010!

That begs the obvious question? With only 3.5% cash what’s left to buy the dip? With over-ownership of the M-7, these stocks aren’t just overbought, a) There’s previous little cash left to buy when the prices get attractive and b) You already own all of them, where’s the room to add more?

We could be in a fading, twilight of a bull run and headed for a correction according to Scott Rubner, managing director for global markets and tactical specialist at Goldman Sachs.

Rubner was categorical in stating the good times from corporate buybacks, retail investors jumping in on every dip, 401k inflows, and beginning of the year investing was waning, and once the corporate buyback period went into the quiet period for Q2, fund flows would move away from equities.

According to Rubner:

“My highest conviction is that this massive ability to buy dip alpha is starting to wane.” Rubner also said that hedge funds have allocated a lot of risk back into the market. Global equities saw the largest net buying in two months last week.

Rubner backed his findings with two key statistics; His assessment that computerized trading desks selling triggers, in the event of a market dip would unload $62Bn worth of equities compared to just $9.55Bn of buying on buying signals – pretty asymmetric towards the downside. Secondly, he also cited “A net retail buy imbalance for the last 22 days, including the top three largest days on record, he said. “This cohort is happy to buy any 2-3% dips for now.”

Q4-24 Earnings weren’t good enough:

The FactSet report on S&P 500 Earnings on 02/14 was just average and for this market to keep rising average won’t do – the valuations The M-7, bellwethers were also sluggish and will have a hard time taking the indices higher.

And while I’m positive about AI, semiconductors, and several fundamentally strong tech companies, valuations have been stretched for a while, thus it would be prudent to take advantage of some of the prices by booking profits, which I have started and posted in the trade alerts section.

While a set of economic indicators doesn’t necessarily doom the market, the downside surprise indicates that we’re not paying enough attention to economic weaknesses, against a backdrop of stretched valuations and interest rates that refuse to fall. The correct de-risking strategy would be to sell and keep cash available for better bargains.

The Fed’s favored inflation gauge – core PCE – cools slightly in November

The core PCE Price Index, the Federal Reserve’s preferred inflation measure, edged up 0.1% M/M in November, less than the +0.2% consensus and cooling from the +0.3% pace in October. Personal income and spending also came in slightly lower than expected in the month.

On a year-over-year basis, core PCE increased 2.8%, just under the 2.9% consensus, and running at the same pace as in October.

PCE Price Index, which includes food and energy, also ticked up 0.1% M/M vs. +0.2% consensus and +0.2% prior.

That measure translated to a 2.4% Y/Y increase, less than the +2.5% consensus, but slightly hotter than the 2.3% rise in October.

Personal income: +0.3% M/M vs. +0.4% expected and +0.6% prior.

Personal outlays: +0.4% M/M vs. +0.5% consensus and +0.4% prior.

At the time of writing, premarket S&P 500 Futures are down 0.6% after being down 1.5% overnight after the second stop-gap funding bill failed miserably to get through the House of Representatives.

The unemployment rate ticked down to 4.2%, as expected, from 4.3% in July.

Nonfarm payrolls rose by 142K in August, accelerating from the 89K added in July (which was revised down from +114K), but still lagging the +160K consensus,

“August #jobsreport is a touch better than July but not by much: the job market is clearly cooling,” said Daniel Zhao lead economist at jobs site Glassdoor in a post on X.

Wages gained more ground than expected in the month, with average hourly earnings climbing 0.4% vs. 0.3% consensus and 0.2% prior On a Y/Y basis, average hourly earnings rose 3.8% vs. 3.7% consensus and 3.6% prior.

“Wage growth moved up a bit to 3.8% from 3.6%, but not enough to get in the way of the Fed’s pre-announced rate cut later this month,” said Brian Coulton, Fitch Rating’s chief economist,

The labor force participation rate was unchanged at 62.7%, matching consensus.

There was a combined 86K downward revision for June and July.

With the weaker-than-expected jobs growth, traders have increased expectations for a 50 basis-point Fed rate cut on Sept. 18, bringing the probability to 47.0% from 40.0% on Thursday. The 25-bp cut probability dipped to 53.0% from 60.0% a day earlier, according to the CME FedWatch tool.

Broader markets are drifting, there’s really nothing in this payroll report that suggests the September swoon is over, I would stay on the sidelines and let the markets correct a little more.

A rate cut could be on the table as soon as September, if inflation continues to progress toward the Federal Reserve’s 2% goal, Federal Reserve Chair Jerome Powell said at his post-monetary policy decision press conference.

In the labor market, supply and demand have come into better balance and have returned to about where they were before the pandemic — “strong, but not overheated,” he said.

Earlier today, the central bank’s Federal Open Market Committee kept its benchmark rate at 5.25%-5.50%, a level that it has stayed at since July of last year.

The second quarter’s data has strengthened confidence that inflation is heading sustainably toward the Fed’s 2% goal, he added. It’s waiting for additional data to further strengthen that confidence before the FOMC reduces the federal funds rate target range.

“We have made no decisions about future meetings, and that includes the September meeting,” he said.

S&P 500 5,022 down 243 points, 4.6% from its all-time high of 5,265.

10-Year US Treasury 4.6%, possibly breaching its Oct 2023 high of 4.98%

There has been a lot of consternation regarding the market in the last two weeks, with the index dropping almost 5% and the 10-year jumping from 4.25 to a high of 4.67% because of the fear of higher for longer interest rates due to stubborn inflation and the reluctance of the Fed to cut rates till they put the inflation genie back in the bottle for good.

Let’s look at it chronologically from Oct 2023.

In late October 2023, when the 10-year was close to breaching 5% Janet Yellen signaled lower interest rates by borrowing $76Bn less than anticipated for the last quarter of 2023. A nod to the nasty run-up in rates, which if unfettered could have been harmful to the economy. The Feds had stopped raising interest rates after the last quarter-point raise in July, and by October, the consensus viewpoint was developing that the markets had done the Fed’s work with the 10-year treasury circling 5%.

Around the same time, multiple Fed officials had said rising Treasury yields are indicative that financial conditions are tightening, possibly making additional rate hikes unnecessary, when the 10-year Treasury yield topped 4.9% on Wednesday, a first since 2007. During this run-up in interest rates, the S&P 500 had dropped to 4,120 from its July high of 4,560.

Once the 10-year treasury topped out, and Q3 2023 earnings season also exceeded expectations it set up the S&P 500 for a furious run up from the October low of 4,120 to about 4,800 by Dec 2023. A massive gain of almost 700 points or about 17%! helped by the Dec dot plot indicating possibly 3 cuts in 2024

We had another positive run in Q1, to the all-time high of 5,265 – both on AI-related earnings and expectations of the 3 cuts materializing in 2024.

My takeaways

A drop of 4.6% compared to the rise from 4,120 in October to 5,265 (28%) is an overdue correction, not a reason to panic.

The earnings yield of the S&P 500 = $245/5,022 = 4.9%, which is just above the 10-year treasury yield of 4.6% – we’re getting just 0.3% higher for a riskier investment compared to a risk-free investment of a government security. That’s a very small risk premium, I would think the S&P 500 is likely to fall further to see some semblance of the historic and mean premium of at least 1 to 1.5%.

The same argument that the Fed used in October is likely to happen as the treasury inches towards 5% –

a) the market itself has made financial conditions worse, (done the Fed’s work – a 0.6% rise in the treasury is more than 2 quarter-point hikes!)

b) Buying a risk-free (US Government) long-duration bond paying 5% is a damn good yield and when funds start buying bonds, the yields fall. There will be buyers from all over the world for that kind of yield. Especially in the event of further turmoil in the Middle East – that’s the flight to quality and safety. I don’t see yields topping 5% – I would be shocked if it did.

The Vix (Volatility Index) or the fear gauge as it is known has shot up to 18-19, after being dormant to steady in the 12 to 14 range through Q1-2024. Computerized trading desks or CTA’s, trade based on volatility which will cause sudden drops and a lot of choppiness, which scares investors. Zero-day options are not helping either. For example, if I see a 1% down day, my first reaction is to lower my buying limits.

Earnings season should be good, but misses are likely to be hammered disproportionately given the weakness in the market. Semiconductor monopoly ASML, which missed bookings but assured the same full-year guidance and a great 2025, dropped 8% today.

The graph below is a good contrarian indicator and makes me shake my head at supposedly professional investors. Fund managers have record low cash levels – they’re overextended at only 4.2% cash. When they need the money to pick up bargains, they don’t have it! Some professionals! This won’t help the market recover easily.

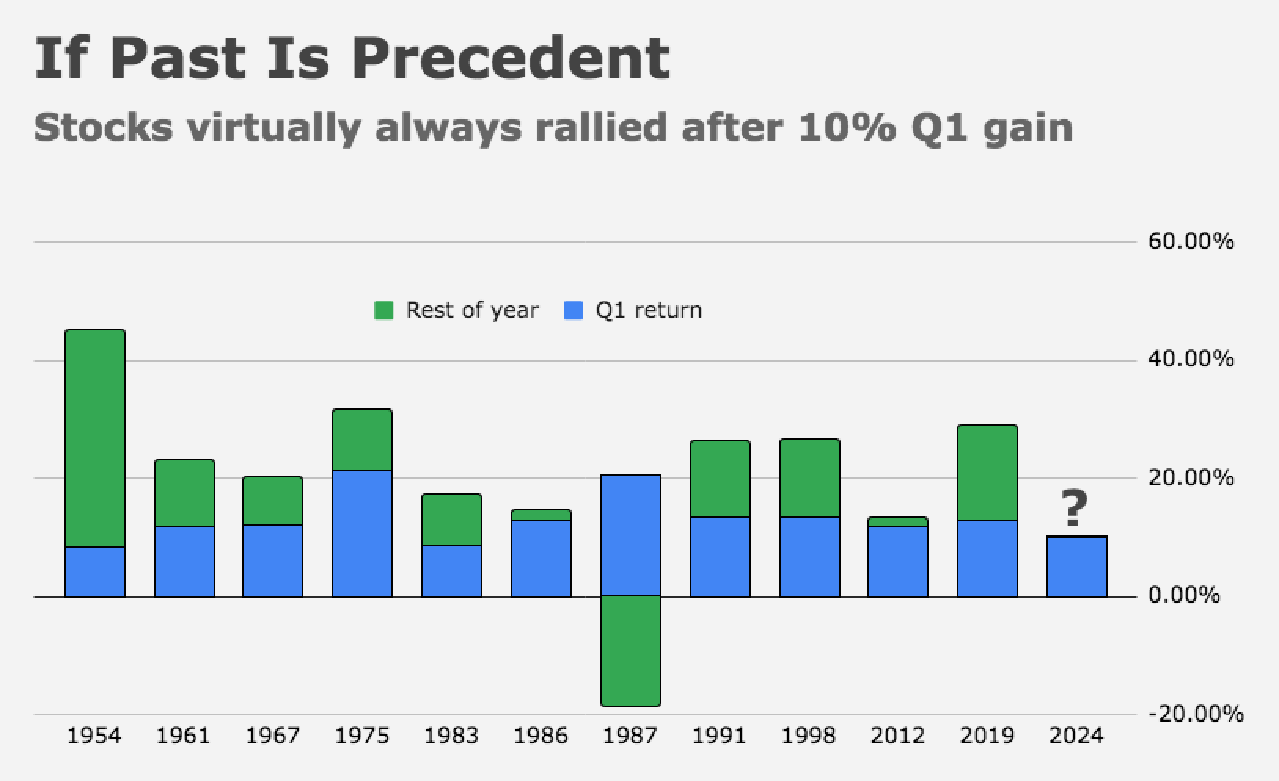

This is another good chart.

If Q1 has risen more than 10%, on every occasion except 1987 (the year of the Black Monday crash) it has closed the year higher. That doesn’t preclude drawdowns and the average pullback in the years was 11%, with a low of 3%.

I feel the best way to play this uncertainty is patience and lower limits – the first quarter was exceptional and unlikely to be replicated.

THE LONG-TERM STORY FOR QUALITY STOCKS IS VERY MUCH INTACT, but we would be better off getting good prices. The first to recover will be the high-level quality stocks – see how steady Microsoft is compared to the rest.

In the last 15 days, my buy trades and recommendations have been limited as you may have noticed and strictly averaging lower with lower limits. I intend to keep it that way.

The 2% Fed target is a myth and highly unlikely to be achieved. Historical CPI has been closer to 3%, and given the move away from globalization, and China decoupling in the past 3-4 years, that era of persistent disinflation is likely to be over. You saw Japan’s move.

That said – At least, I believe that beyond a certain point Fed induced higher interest rates will not name inflation, a lot of US inflation is fiscal, not monetary, the Feds know that and will cut for sure as insurance – nobody wants to derail the economy. I still think the three cuts of 25% each in 2024 are achievable. But to your point, yes, I don’t think we’ll go below a 3.5% treasury for a long, long time. I agree with energy stocks doing better in 2024, they will take up more space in the index.

The 10 year treasury dropped from a high of 4.195 on 1/25 to 3.942 today, 01/31 – the day the Feds and Chair Powell was clearly signaling no chances of a rate cut at the March Fed meeting.

Intuitively the yields should have gone up – is there something else at play.

I believe Yellen’s dovish nod on 1/29 was the main catalyst for the drop in rates and clearly that seems to be overriding Chair Powell’s comments after the FOMC meeting.

Simply, if the government decides it needs to borrow more, it doesn’t get to borrow at cheap rates; the private sector will naturally charge more, which means interest rates go up. Now if Powell’s boss signals that borrowing will be a) less than anticipated this quarter b) borrowing intervals and amounts will be regularly spaced out, it’s a clear dovish signal that the government doesn’t want interest rates going up in an election year.

From 2017 to 2021, Upstart grew at a frenetic pace of 70%, before higher interest rates, funding constraints and higher defaults led to a massive decline in revenue.

Upstart was supposed to be an agnostic “Fintech” marketplace without credit exposure, but they made the mistake of taking auto loans on their books, which completely negated the buying/bullish case.

Upstart has boosted its capital but even at its latest earnings call, management stated Upstart’s ability to approve borrowers is constrained due to a macroeconomic environment of low consumer savings and high credit default rates.

Right now revenue growth forecasts are low and there are no clear indications of a turnaround – sure lower interest rates and better participation from banks and other financial institutions could be tailwinds in the second half.

Interestingly, while researching this one, I looked at Sofi Technologies (SOFI) and Pagaya (PGY), which are in much better shape, much more resilient and could be winners. Pagaya has executed well in the high interest rate downturn. Both are on the riskier side, and I will update later today.