Terrible history of losses, unproven technology, poor execution and shareholder unfriendly because of constant dilution to raise cash.

High risk of Obsolescence

Technological advancements in next generation Electrolyzers offer more hope for a green hydrogen economy,

Incumbent Electrolyzer producers like Plug Power are at a disadvantage due to technological inefficiencies and financial instability, making them a risky investment.

Hydrogen can be an alternative source of energy, but Plug may not be the right player, its conversion efficiency is supposedly lower in the 75% range compared to newer technologies offering 95%.

I remember this now; it came out with this headline – Serve Robotics skyrockets as Nvidia takes stake.

It’s an UBER spin off with robots for food delivery or other consumables, was going nowhere till the Nvidia stake was disclosed, which they bought from an early investment in a convertible primary note. The stake is about 10%. Interestingly, two others have investments as well including 7-11, and Delivery Hero based out of Germany.

Delivery Robots could work for the last mile, there is potential and its similar to drone delivery.

This business will need a lot of cash to stay alive and keep developing robots so another big risk is dilution – they will have to keep coming to the market and issuing shares for funding needs.

Its hugely speculative and risen from $2.50 this year, if one caught it early around 4 a tiny speculative position wouldn’t have been bad, on a bad day this one could easily drop 50%.

June revenue at Alphabet grew 5% sequentially from March to $84.3 billion, a 13% year-over-year rise and a bit of a deceleration from March’s 15.4% year-over-year rise.

Q2 GAAP EPS of $1.89 beats by $0.04.

At $180, Alphabet is priced at only 21-times 2025 earnings. Very reasonable for a member of the M-7, search market leader, AI pioneer, and owner of You-Tube.

Why is it down post earnings: WSJ’s title was apt Google Fails to ‘Wow’ as AI Bills Mount

Overall revenue exceeded Wall Street’s consensus projection by just 0.6%—the lowest beat percentage in at least five years,

Capex = $49Bn for the year, this was mostly expected but still got a thumbs down, because depreciation will hurt the bottom line.

Google has to spend to keep up – it doesn’t have a choice.

“Look, obviously we are at the early stage of what I view as a very transformative area,” Alphabet Chief Executive Sundar Pichai “the risk of underinvesting is dramatically greater than the risk of overinvesting for us here,” not mentioning the record amounts of capex that tech rivals Microsoft, Amazon and Meta Platforms are pouring into the same thing.

Rejected Alphabet’s bid for $23Bn – I think that’s actually good for Google, at 46x current year sales. Granted this would have given them a considerable leg up in cybersecurity – but is a $500Mn revenue company, which would never move the needle for the behemoth.

I own GOOG, and plan to hold for a long, long time, it’s been recommended on several occasions here. I could buy more if the price drops but given the change in sentiment towards big tech I’m happy to sit on the sidelines for a bit.

There seems to be an inflection point – the rate of growth is going to get lower on tougher comparisons and therefore there is more hesitation to buy at inflated levels.

Revenue missed by about 2% ($440Mn miss on $21.8Bn revenue). Revenue dropped 1.4% YoY, indicating that economically sensitive cyclicals are still having a hard time. FedEx too, expects just 1.8% growth for the second quarter. UPS’ earnings miss was 10% – that hurt the stock more, its down 10% premarket to $130.

For the past 3-4 weeks there has been a steady drum beat to get out of expensive tech to companies that could benefit from lower interest rates and cheaper valuations.

The 10% drop in UPS due to the big earnings miss and the lack of growth underscores how difficult it is to find and invest in the right cyclical. Avoid the value traps and be very discerning in finding the right company or index.

TSM hit it out of the park last week, confirming that the high-performance semiconductor sales are doing extremely well.

Q2 revenue growth of 32.8% y/y and net income growth of 29% y/y.

Q3 expected to set another revenue record on strong AI and smartphone demand, full year guidance raised. Full Year expectations are for 28% and 24% earnings growth to $6.4 per share.

3Nm (the most advanced node powering Nvidia, Apple, etc.) revenue was 15% of sales. Nvidia’s not the only company with higher prices, they in turn pay TSM quite well for 3Nm processing! 5Nm also went to 35% of sales – the two now dominate TSM sales with 50%.

If TSM didn’t have geopolitical risks from China, and Trump demanding payments for protection didn’t help either, this would have been easily 40x earnings, over $250 per share. given the technological and market share lead. Overall, TSMC should continue to dominate in advanced process nodes and high-volume manufacturing for many years.

I had sold 20% around $183 last June, but am going to hold on to the rest, there’s really nothing much we can do with Chinese tensions – if there are nasty developments from that front, we’ll have much bigger problems than the price of TSM!

This is an electric bike maker from Thailand, with a tiny market cap of $37Mn. The company’s debut product, the i300, is a high-performance electric “perfect city bike” with widespread acclaim, including winning the prestigious Red Dot Product Design Award, the German Design Award, the Australian Good Design Award, and other E-Mobility awards.

The value proposition – Price around only $10,000 lightweight motor, rechargeable and removable battery pack.

Weaknesses and challenges

Pre revenue, development stage company with a limited operating history as a public company, Product development in new category in this cyclical and volatile sector is notoriously costly, and their planned entrance to the U.S. market will require considerable capital, effort, and time.

In addition, the sobering fact is that the i300 has been in development for almost six years (admittedly the COVID-19 crisis was a legitimate factor in this delay) and can only be ordered online at the company website at Zapp i300 Urban Electric Scooter/Motorbike | Zapp EV.

Two competitors at an advanced stage:

Livewire (LWR) – Market cap of $1.7Bn

LVWR has a strong strategic relationship with Harley-Davidson (HOG) which spun off its electric motorcycle division on 9/20/22 as a separate, publicly traded company in a SPAC deal. LVWR has retail partners in more than a dozen states in the U.S, and sales of only $38Mn, 18% lower than 2022, but is expected to grow 30-40% in the next 3 years.

Niu Technologies (NIU), with over 400 retail stores in the U.S. through retail partners is another strong competitor with a market cap of $165Mn and revenues of $479Mn with 20% growth prospects.

ZAPP’s lack of experience to produce at scale and shareholder dilution are two other weaknesses.

I suspect that the 15% rise was due to short covering, this was quite heavily shorted. I want to take a close look at the Niu.

Galapagos (GLPG) $27 pivots to CAR-T therapy, divesting Jyseleca; faces clinical, market risks amidst investor skepticism. Divestiture of its Jyseleca business reflects a significant shift in its business strategy. There are dissenting opinions on whether this was a good move.

Revenue up 9% YOY; operating losses reduced; strong cash reserve at $4.2B;

Negative enterprise value and underperforming stock; high short interest and bearish investor sentiment.

A lot of uncertainties in CAR-T strategy, competitive landscape, and market skepticism. The CAR-T therapy landscape is intensely competitive, and the success of Galapagos’ key candidates, GLPG5101 and GLPG5201, is imperative.

Pipeline and R&D Success Rate: Concentrating on CAR-T therapies, particularly GLPG5101 and GLPG5201, presents significant risks. Nevertheless, the EUPLAGIA-1 study’s preliminary data reveals encouraging results. In the study, 75% of CLL patients (12 out of 16) who received GLPG5101 achieved Complete Response with no report of serious adverse effects. In contrast, the GLPG5201 treatment group faced more severe outcomes, with 2 out of 14 patients encountering fatal (Grade 5) events, and a few others experiencing life-threatening or disabling (Grade 4) complications.

This is from a biotech analyst, he’s bearish but a couple of other biotech specialists were bullish in 2023, but haven’t published any updates.

Apple started its Developers Conference with its long awaited, long overdue AI development announcements yesterday.

These were the key points

Emphasis on privacy – Majority usage of AI on device but cloud available as well for more computing power, they would be using their own cloud service instead of Google or Microsoft. Apple will be hosting its own Cloud AI services on its own Apple Silicon servers to counter Microsoft’s cloud AI.

Strategy was integration and not an add on – To show AI integrated into the apps and products you already use—rather than powering a tacked-on perk or stand-alone chatbot.

Partnering with Sam Altman’s OpenAI – Not developing their own artificial intelligence from scratch, instead partnering with Sam Altman’s AI, but crucially it will be integrated. Using a third party for AI could be a smarter move (cheaper, less Capex, fewer failures) – or simply they were too far behind.

Integration Apple’s strongest differentiation was and remains integrated hardware and software product, “System on chip” – basically Apple created and designed silicon with its own operating system and hardware, it’ll be interesting to see how well it is integrated.

The adoption is companywide and includes iOS 18, iPadOS 18 and MacOS Sequoia, Siri,

Some new features, and a lot of catching up – – several features are in Google and Samsung.

Playing Catch Up – Writing tools, Voice transcription, Image generation and Notifications, these all exist, and are now available from Apple Intelligence.

Differentiators

The key differentiator here is that Apple Intelligence will also make it easier to search through our existing data – for example, What’s exciting here is the blending of AI with the photos we’ve already taken, and prioritize our notifications. Like other chatbots, you can now text with Siri. But unlike other chatbots, Siri has access to all your Apple stuff. When all the promised updates arrive, it will be able to see what’s on your screen and work across apps. “Add this address to his contact card.” “Text yesterday’s picnic photos to my mom.” Things like this make total sense to a human but up until now have been out of Siri’s reach. The thing that really elevates Siri is its new friend, ChatGPT. When you ask Siri to do some things it doesn’t know how to—say, come up with dinner ideas based on your recent grocery haul—it asks your permission to check with an integrated version of OpenAI’s bot. However, If Apple can pull off what it showed and convince people that Siri is no longer painfully stupid, it might be a tech miracle. That’s a big if. The company has a decade long history of underwhelming Siri improvements.

If you get a chance watch Joanna Stern’s video in the Wall Street Journal.

Apple AI analysis: Impact on the company’s business and stock.

Much needed, frankly regardless of much this helps Apple, if they hadn’t done this it would have hurt them really badly.

Apple’s widest moat has been its integration unlike its competitors, for example you have Windows operating, Intel Silicon and Dell hardware – the Wintel systems for the mass market competing on price. Or the Samsung phones with the Android operating system. Apple’s was always designed to be one seamless product from scratch and that’s how they got their premium pricing and loyal customers.

They continue to emphasize integration and privacy with AI, a big plus.

I think overall, this will help and Apple is going add on features with each new iPhone or Mac version and increase sales, which were stalling for the past three years.

For a lot of people, yes may be underwhelming and just catching up for the regular Apple user, it would be a convincing argument to at least stay with Apple and possibly upgrade.

A core holding: I’ve bought and held Apple for several years now, and usually buy on declines, the last buy call I had made was around $170, and will add if there are unusual or large dips, this will remain a core holding for at least another 5 years. Apple is not a big mover but I’m very, very confident of at least 10-12% a year, plus it works well as a defensive stock too in bad times.

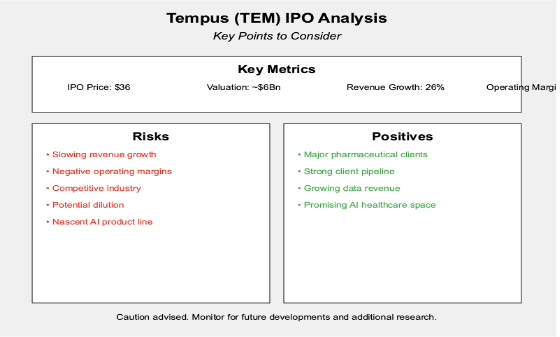

Revenue growth has slowed to 26% from 65% and likely to end the year at $650Mn.

The valuation is about $6Bn almost 10x sales with negative operating margins of 37%.

Gross margins are also lower this year than last year, which is a bad sign.

I won’t reject paying 10x sales if the growth is extremely strong, say over 40% but only 26% growth pre-IPO doesn’t inspire much confidence, especially when they’re so far from profitability.

Dilution Risk – in the first few years post IPO, cash will needed to fund losses and there will more dilution.

Very competitive industry – there are several large companies doing a combination of diagnostic revenue, data sales and getting paid for drug discovery milestones.

The AI product line is nascent – less than $3Mn in revenues in Q1-24.

Major investors – Softbank, Baillie Gifford, Google is a convertible note holder. Eric Lefkofsky – Founder, also co-founded Groupon and Mediaocean.

Positives

They do have major pharmaceutical clients – the roster is pretty impressive, and the pipeline is also strong. Some areas of promise – revenue from data has picked up, which can be more stable and sustainable.

To be sure, this is a very interesting and promising space and has a genuine need for AI related solutions. For now, I would be a little careful, there doesn’t seem to be enough growth, differentiation, or compelling reasons to invest, unless the price is really low. Wouldn’t want to get caught up in the first day euphoria. I’ll keep a lookout, there will be more research coming down the pike.

Dropbox (DBX) $21.25 – I’m Neutral On This Company

Dropbox has been quite the underperformer, in the last 5 years the stock has lost 7%, and 8% in the past year.

Sales growth has really slowed down from 8-10% to only 3-4% expected for the next 3 years and that’s why there’s no appreciation for the stock. Its a fairly profitable company 15-16% operating margins and cash flow of 30+% because of the high stock-based compensation. Earnings growth is also tepid with just 6-8% expected for the next three years. These are two big reasons why there isn’t much scope for Dropbox to grow.

Dropbox is proving to be less sticky than originally thought. As churn rates have increased over the past year, many investors are re-evaluating the stickiness and value of Dropbox’s subscription revenue base.

Deep competition- Dropbox has always been in an eternal tug-of-war with competitors Google Drive (which has an advantage in pricing and integration with consumer email accounts) and Box, Inc. (BOX), which is better known for its enterprise-grade features and security.

Confidence in Dropbox faltered even more after the company reported rather dismal Q1 results – Analysts have an average hold rating.

Box (BOX), which is about 40% the size of Dropbox, not surprisingly, has a better growth profile with 6-7% revenue growth and 11-12% earnings growth expected in the next 3-4 years. It has a similar valuation multiple, so it’s not like that the markets have given it too much of a premium.

The main thing is that growth will likely be in the low to mid-single digits in this industry, so can’t expect too much in terms of return from either.

The one thing Dropbox/Box could do is to put their cash to better use (both generate in excess of 30% cash margins) and buyback shares, the valuations are low enough, which would help them and also help investors. For now, its neutral – don’t see much scope for expansion.