Intel’s (NASDAQ: INTC) significantly weaker-than-expected guidance for the coming quarter overshadowed better-than-expected first-quarter results.

For the coming second quarter, the Pat Gelsinger-led firm expects revenue to be between $12.5B and $13.5B, well below the $13.61B analysts were anticipating.

It also anticipates earning an adjusted $0.10 per share with adjusted gross margins of 403.5% and a tax rate of 13%. Analysts were anticipating adjusted earnings of $0.25 per share.

Shares fell more than 6% in extended-hours trading.

For the period ending March 30, Intel earned an adjusted $0.18 per share on $12.7B in revenue. The quarter is Intel’s first period in changing its reporting structure to focus more on its foundry business. Intel products, which now include client computing, data center, and network and edge, came in at $11.9B, including a 31% year-over-year rise in Client Computing revenue to $7.5B.

Datacenter and AI revenue came in at $3B, while revenue attributed to Mobileye (MBLY) was $239M, down 48% year-over-year. The Network and edge segment generated $1.4B, while the company’s foundry segment saw revenue decline 10% year-over-year to $4.4B.

Analysts expected a year-over-year increase in both the top and bottom lines, with the Pat Gelsinger-led firm expected to earn $0.14 per share on $12.78B in sales.

A consensus of analysts expected Intel to earn an adjusted $0.14 per share on $12.78B in revenue.

Quantum computing is still in its infancy and a difficult and risky endeavor. The scale that quantum computing wants to achieve – 3.6 billion GPUs would be required to simulate a 64-qubit system. To do this in a commercially successful way at scale will take a lot to go right.

Several methods are competing with one another:

Solid state is used by the likes of Google, IBM, and Rigetti Computing (RGTI) to use artificially manufactured qubits that are engineered into the system.

Exploiting naturally occurring substrates (photons or atoms) that exhibit quantum properties. This method is used by Quantum Computing (QUBT)

Trapped atomic Ions – IonQ’s methodology uses trapped atomic ions as qubits to construct quantum computers.

None of them have had much commercial success, but are seeing orders and bookings.

IonQ – has a $ 25Mn grant/order from the US Air Force.

Total revenues for 2024 = $42Mn and 2025 = $82Mn

Achieving the 64-qubit system in 2025 is a must-reach milestone for IonQ, simply to have a shot at commercialization or even survival.

The big negative besides the commercialization risks is that the two founders have left – for academia, though not for competitors.

It has cash of $460Mn so will survive through 2027.

No system has achieved a broad quantum advantage – where developers prefer quantum computers to traditional ones – it could be three to five years on the horizon/ or not at all

Quantum wants to combine GPUS, networking, and AI, but hardware and software innovations have to produce systems economically at scale, as well as demonstrate to enterprise-level customers why it needs a quantum computer.

A LOT OF IFS — of competing systems, need to preserve cash, race to innovate, race to scale operations, and do we even need quantum computing?

Bottom line – this is like a biotech or a drug discovery bet, high risk/high reward.

Post earnings the markets punished it 20% for a marginally weaker guidance and higher than expected CAPEX. Pre-earnings the stock had been up 130% for the past year, so this 20% drop was perhaps, overdue.

Rev beat of 36.46Bn v 36.12Bn 27% YoY – but too little a beat.

Rev guidance 36.5Bn to 39Bn or a midpoint of 37.75 V 38.24, still 18.5% YoY growth but too much of a miss.

Capex is higher at 37.5Bn midpoint now V 33.5Bn – bad for Meta but good for Nvidia/AI most of the Capex is for AI.

META has a GAAP operating profit margin of 49% in the family of apps business – that’s a phenomenal margin, but it drops substantially because of losses in the Reality Labs business. Still, its company-wide margin was 38% – a 52% increase YoY.

Will parse through the earnings call/analysts’ upgrades tomorrow morning, the selloff may be overdone.

The weaker manufacturing sector is a much smaller part of the economy than services. Manufacturing PMI seems to suggest that economic growth and inflation are not as strong as feared – especially if payroll declines are true to this estimate at least. This is not a major surprise, but the weakness in the service index shows that services is seeing a spillover. This should be watched carefully.

The markets have reacted positively, following yesterday’s bounce back – up ¾ to 1%. (Bad news is good news!)

Tesla reports today, likely to be bad but may be discounted.

Meta reports tomorrow after the market, I’ll put up the preview numbers.

Microsoft and Google report on Thursday.

To round off the week we have the PCE number on Friday, which should give us a better idea of inflation – that is the Fed’s preferred gauge.

U.S. PMI Manufacturing unexpectedly slips into negative territory in April

April PMI Manufacturing Index: 49.9 vs. 52.0 consensus and 51.9 in March. The services PMI did, too, slip to 50.9 (vs. 52.0 expected) from 51.7 a month ago, though it remained in positive territory, with the index still above 50.

The composite PMI (flash estimate) came in at 50.9, down from 52.1 in the previous month, signaling business activity in the U.S. expanded at a slower pace during the month, in the wake of signs of weaker demand.

The group’s measure of employment slid 3.2 points to 48, reflecting shrinking services payrolls and slower growth at manufacturers. The composite index of prices received, meanwhile, pulled back from a 10-month high.

“The more challenging business environment prompted companies to cut payroll numbers at a rate not seen since the global financial crisis if the early pandemic lockdown months are excluded,” Williamson said.

The decline in the employment measure suggests companies see current capacity as sufficient to handle demand. Order backlogs remained in contraction territory during the month.

New business at service providers shrank for the first time since October, with some firms indicating higher borrowing costs and still-elevated prices were limiting demand.

The overall index for services activity decreased to the lowest level in five months, while the manufacturing PMI showed a slight contraction.

“Further pace may be lost in the coming months, as April saw inflows of new business fall for the first time in six months and firms’ future output expectations slipped to a five-month low amid heightened concern about the outlook,” said Chris Williamson, chief business economist at S&P Global Market Intelligence.

Reasons for the lower revenue: Reduced vehicle average selling price (ASP) YoY (excl. FX impact), an unfavorable product of the mix, and a decline in vehicle deliveries, partially due to the Model 3 update in the Fremont factory and Giga Berlin production disruptions.

A negative FX impact of $0.2B1 + growth in other parts of the business + higher FSD revenue recognition YoY due to the release of the Autopark feature in North America.

Beneath all that – Total revenues are lower by 9% YoY, and auto revenues are down 13% YoY. Energy and service revenues are keeping the flag flying still.

The stock is holding up at $154 – I guess it wasn’t worse than expected.

There are some fears of the lack of transparency for the next quarters till analysts and investors get used to not seeing subscriber numbers, but operating margins are improving further, revenues are guided to 14% mid-point growth and earnings should increase 25% per year in the next 3. The stock is down 13% from its all-time high.

Netflix Q1-2024

Beats all around, and has better guidance as well.

GAAP EPS of $5.28 beats by $0.76.

Revenue of $9.37B (+14.8% Y/Y) beats by $90M.

Global streaming paid memberships: +9.33M to 269.6M. UP 165 YoY, Q1 is seasonally low, and in Q1-23, the YoY growth was inly 4.9% so this is quite impressive.

Q2 Guidance: Revenue of $9.49B vs. $9.28B consensus, 16% growth, 21% F/X neutral growth.

EPS of $4.68 vs. $4.54 consensus.

For the full year 2024, we expect healthy revenue growth of 13% to 15%, based on F/X rates at the end of Q1’24.

We now expect an FY24 operating margin of 25%, based on F/X rates as of January 1, 2024, up from our prior forecast of 24%.

S&P 500 5,022 down 243 points, 4.6% from its all-time high of 5,265.

10-Year US Treasury 4.6%, possibly breaching its Oct 2023 high of 4.98%

There has been a lot of consternation regarding the market in the last two weeks, with the index dropping almost 5% and the 10-year jumping from 4.25 to a high of 4.67% because of the fear of higher for longer interest rates due to stubborn inflation and the reluctance of the Fed to cut rates till they put the inflation genie back in the bottle for good.

Let’s look at it chronologically from Oct 2023.

In late October 2023, when the 10-year was close to breaching 5% Janet Yellen signaled lower interest rates by borrowing $76Bn less than anticipated for the last quarter of 2023. A nod to the nasty run-up in rates, which if unfettered could have been harmful to the economy. The Feds had stopped raising interest rates after the last quarter-point raise in July, and by October, the consensus viewpoint was developing that the markets had done the Fed’s work with the 10-year treasury circling 5%.

Around the same time, multiple Fed officials had said rising Treasury yields are indicative that financial conditions are tightening, possibly making additional rate hikes unnecessary, when the 10-year Treasury yield topped 4.9% on Wednesday, a first since 2007. During this run-up in interest rates, the S&P 500 had dropped to 4,120 from its July high of 4,560.

Once the 10-year treasury topped out, and Q3 2023 earnings season also exceeded expectations it set up the S&P 500 for a furious run up from the October low of 4,120 to about 4,800 by Dec 2023. A massive gain of almost 700 points or about 17%! helped by the Dec dot plot indicating possibly 3 cuts in 2024

We had another positive run in Q1, to the all-time high of 5,265 – both on AI-related earnings and expectations of the 3 cuts materializing in 2024.

My takeaways

A drop of 4.6% compared to the rise from 4,120 in October to 5,265 (28%) is an overdue correction, not a reason to panic.

The earnings yield of the S&P 500 = $245/5,022 = 4.9%, which is just above the 10-year treasury yield of 4.6% – we’re getting just 0.3% higher for a riskier investment compared to a risk-free investment of a government security. That’s a very small risk premium, I would think the S&P 500 is likely to fall further to see some semblance of the historic and mean premium of at least 1 to 1.5%.

The same argument that the Fed used in October is likely to happen as the treasury inches towards 5% –

a) the market itself has made financial conditions worse, (done the Fed’s work – a 0.6% rise in the treasury is more than 2 quarter-point hikes!)

b) Buying a risk-free (US Government) long-duration bond paying 5% is a damn good yield and when funds start buying bonds, the yields fall. There will be buyers from all over the world for that kind of yield. Especially in the event of further turmoil in the Middle East – that’s the flight to quality and safety. I don’t see yields topping 5% – I would be shocked if it did.

The Vix (Volatility Index) or the fear gauge as it is known has shot up to 18-19, after being dormant to steady in the 12 to 14 range through Q1-2024. Computerized trading desks or CTA’s, trade based on volatility which will cause sudden drops and a lot of choppiness, which scares investors. Zero-day options are not helping either. For example, if I see a 1% down day, my first reaction is to lower my buying limits.

Earnings season should be good, but misses are likely to be hammered disproportionately given the weakness in the market. Semiconductor monopoly ASML, which missed bookings but assured the same full-year guidance and a great 2025, dropped 8% today.

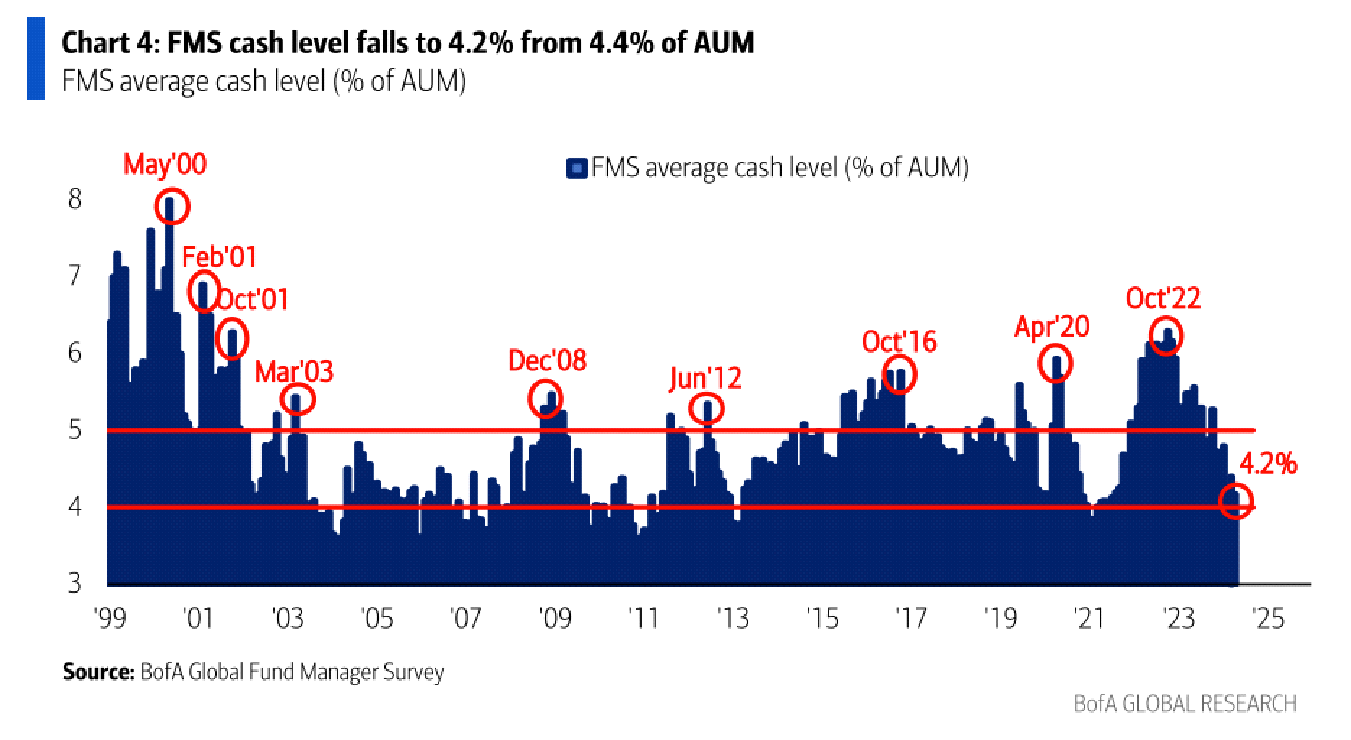

The graph below is a good contrarian indicator and makes me shake my head at supposedly professional investors. Fund managers have record low cash levels – they’re overextended at only 4.2% cash. When they need the money to pick up bargains, they don’t have it! Some professionals! This won’t help the market recover easily.

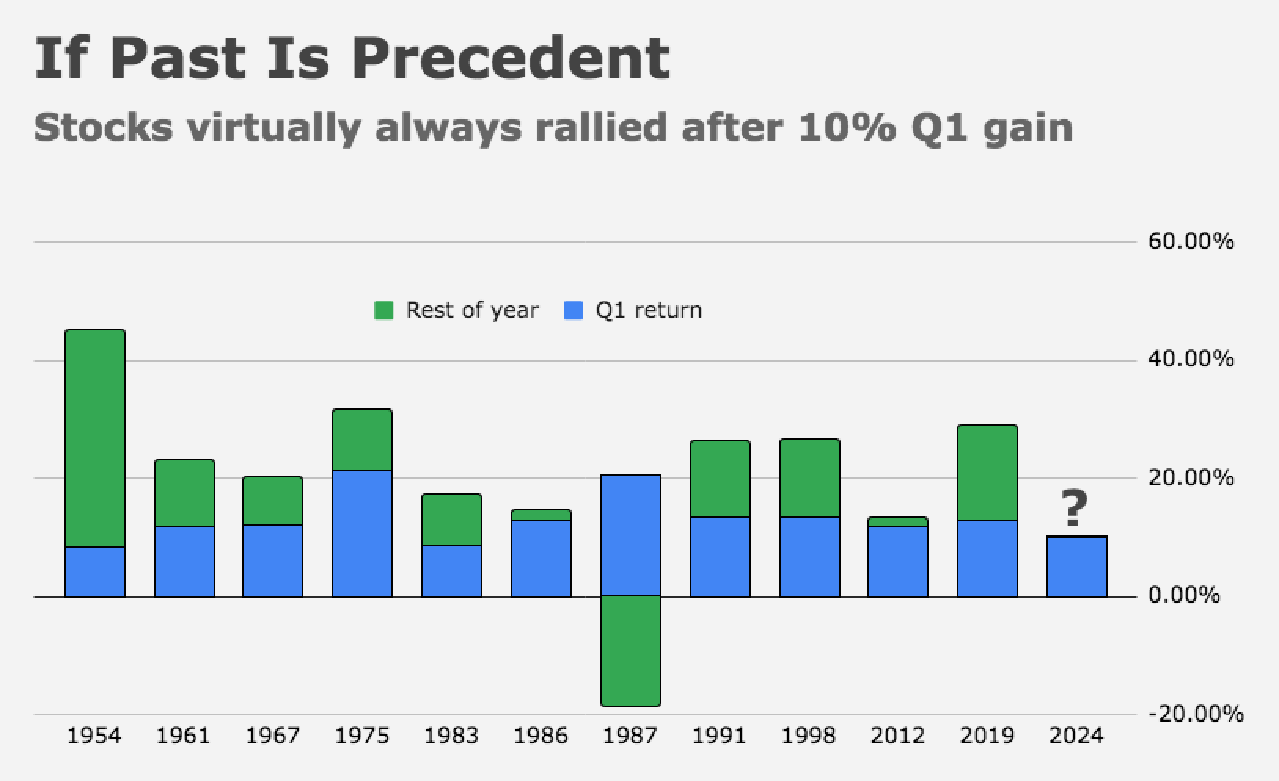

This is another good chart.

If Q1 has risen more than 10%, on every occasion except 1987 (the year of the Black Monday crash) it has closed the year higher. That doesn’t preclude drawdowns and the average pullback in the years was 11%, with a low of 3%.

I feel the best way to play this uncertainty is patience and lower limits – the first quarter was exceptional and unlikely to be replicated.

THE LONG-TERM STORY FOR QUALITY STOCKS IS VERY MUCH INTACT, but we would be better off getting good prices. The first to recover will be the high-level quality stocks – see how steady Microsoft is compared to the rest.

In the last 15 days, my buy trades and recommendations have been limited as you may have noticed and strictly averaging lower with lower limits. I intend to keep it that way.

This is a speculative trade article from an analyst on Seeking Alpha, looking for a short covering bounce, so keep that in mind, when you make your decision.

Globe Life did get a positive report this morning from an analyst, Edward Vranic on Seeking Alpha, suggesting that there would be enough short covering and likely winding up of the speculator’s positions, since they have achieved their short target of $64.

Like most professional short sellers Fuzzy Panda, has used all the alleged corrupt practices at Globe Life to paint a negative picture. As the analyst writes, they didn’t compare it to Primerica, which has a similar problem, and this could be an industry problem.

Policies Written for Dead and Fictitious People.

Forged Signatures.

Funds Withdrawn from Consumers’ Bank Accounts without Approval

Fictitious Bank Accounts are used to Fund Numerous Fake Policies, so Agents hit their bonuses.

Quoting from the report

Fuzzy Panda held a $64.35 price target. GL has dropped below that mark.

GL now has valuation metrics well below the industry average and significantly below PRI, it’s most directly comparable as a life insurance company with an MLM sales structure.

I believe that the stock price will bounce back to $80 or higher due to short sellers covering their positions and bullish investor speculation.

What Fuzzy Panda managed to do was paint GL as a dysfunctional organization filled with frat boys and “crypto bro” types that undertake aggressive sales tactics, show off online, and engage in perverse and questionable behaviors. What it didn’t do is assess how much of this is outside of an industry standard. It wouldn’t be the first time that 25-year-old men out of college bragged about their $100,000 cars, and the company leveraged that as a recruitment tactic. Isn’t the whole point of a growing company to make itself appealing? Should GL be punished for being more honest and upfront about the type of people it believes will do well in selling insurance at its company? If there is something wrong with it, then where are the regulators? Not just over the past five years, for when Fuzzy Panda believes this behavior at GL has accelerated. But over the last 100 years, when a rich lifestyle and fast cars as a financial products sales guru was portrayed as an American dream.

The behaviors undertaken by certain employees and management teams of life insurance companies have been unfortunate. However, up until today – and even in the case of GL up until April 11th – few people on Wall Street cared. For whatever reason, the market reaction was quite pronounced on Fuzzy Panda’s report. Even though it was essentially an aggregation of previously disclosed and/or publicly accessible information along with the opinion of a handful of self-proclaimed experts and investigators. I think that reaction went too far, leading to a speculative buying opportunity on GL.

Fuzzy Panda and associates will cover their shorts. Short interest was 2.75 million as of March 28th and short-marked volume was over 2.2 million between that date and April 10th. It was over 5 million on April 11th, the day of the report. Some shorts are likely already covered on April 12th. One report shows that a significant put option position was opened, and then closed on the 11th. I believe that momentum will continue into this week as the remaining shorts who shorted high will take their profits, while those who are late to the game and entered in at a low price will be squeezed. I remind readers that Fuzzy Panda’s “generous” target was $64.35. Unlike other short reports I have seen, it did not quantify an impact of any potential restatements of financials nor come up with a target of $0 or close to it. Given the relative softness in terms of price targets compared to other reports I have seen, I believe that this firm will be more likely to take profits than to push the narrative for more gains at a lower price.

Therefore, $80 is a reasonable near-term speculative price target on GL and I have positioned myself accordingly.

Here is the link if you want to read the full article.

Two Wall Street firms Wells Fargo and Morgan Stanley have similar advice to what I gave about Solventum in my earlier post. Growth concerns will keep the stock flat.